Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty

Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026

ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026

It was then, when EURUSD was about to breach the 1.40 mark to the upside in the spring of 2014 the ECB took action as well, at the time it was first of all Mario Draghi who ended the rise with the help of verbal interventions. Consequently, EURUSD eased to 1.05 until early 2015. Likewise, a strategy now seems to be emerging in the minutes of the meeting of 19th - 20th July.

The first point is that levels around 1.14 (this is where EURUSD traded at the time of the meeting in July) caused the exchange rates to be an issue for the ECB. That is the case as long as one assumes that the minutes (which of course are not the verbatim transcript) were not “re-adjusted” as a result of the recent EUR strength.

Secondarily, let’s shed some light on the minutes about EUR strength. They point-out that the development up to the July meeting was partially due to the positive fundamental data compared with other currency areas. Moreover there is no mention of concerns about a strong EUR but about the exchange rate overshooting. This concern is not unfounded. USD faces a tough time as a result of Trump and the ECB will soon have to explain to the market that it is going to end the assets purchasing programme.

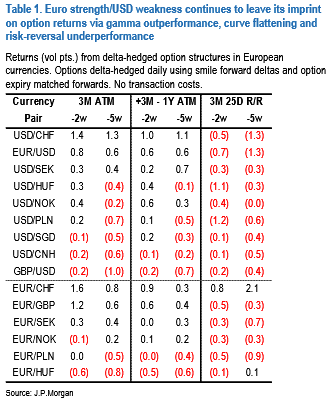

While JP Morgan ponders that the powerful beta-forces of Euro strength and dollar weakness continued to leave their imprint on FX vol surfaces for another week. Gamma continued to outperform, led this time around by the outsized 2.5% w/w move in USDCHF, vol curves remained under flattening pressure and the recent trend of risk-reversals reshaping away from USD calls in favor USD puts stayed intact following a dovish-leaning FOMC statement (refer table).

Realized vols may cool a tad from here as the event calendar eases from here on out till late August, but we are of the view that front-end vols will stay well-supported as (a) August in general tends to be a seasonally strong month for volatility, and (b) investors seem inadequately invested in the bullish Euro trend judging from the breadth and intensity of spot rallies and counter-conventional spot-vol correlations so far, so directional option demand is likely to remain robust.