U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

GBP’s performance ranks mid-table over the past month (+0.5% vs USD, -2.5% vs EUR) as the global impact of the coronavirus has come to dominate GBP's local difficulties with Brexit. But even though Brexit is now being overshadowed by an even more existential crisis, this doesn’t let GBP off the hook, far from it actually, as the accelerated removal of GBP's interest rate support as the BoE prepares to respond to the COVID-19 shock will further undermine the sustainability of the UK's worst-in-class current account deficit (a 4-5% of GDP current account gap is incompatible with the UK's new reality as a low-growth, low-yielder). In addition, while Brexit is being overshadowed, this is only temporary and GBP remains vulnerable from a great sense of realism amongst investors about the government's objectives for the EU trade talks and its credible threat still to walk away in the pursuit of regulatory autonomy from the EU and freedom from strict level playing field commitments.

As a result of the Brexit-virus one-two we are lowering the GBP forecast. The point of maximum jeopardy is expected to be around mid-year as the trade talks reach their make-or-break point (remember that the government has legally barred the transition period from being extended beyond end-2020) and the risk of no- deal crescendos.

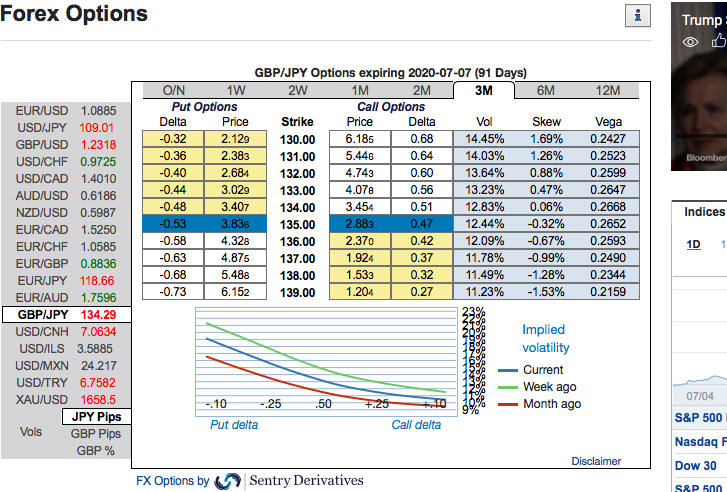

The GBPJPY has been volatile, edging higher briefly to just shy above $134.250 after bottoming out at 123.991 level, the reports of a Brexit deal agreement have also cushioned. Currently, trading with little exhaustiveness due to pandemic turmoil, still, it is well up from last week’s lows.

Even so we believe it worthwhile increasing our bearish beta to GBP through re-selling GBPJPY (our single most successful trade to date this year).

OTC outlook and Hedging Strategy: The implied volatility of this pair that display the highest number among entire G7 FX universe.

While the positively skewed IVs of 3m tenors signify the hedgers’ interests to bid OTM put strikes up to 130 levels (refer above nutshell).

Accordingly, put ratio back spreads (PRBS) are advocated on the hedging grounds. Both the speculators and hedgers who are interested in bearish risks are advised to capitalize on current abrupt and momentary price rallies and bidding theta shorts in short run, on the flip side, 3m skews to optimally utilize delta longs.

The execution: Capitalizing on any minor upswings , we advocate shorting 2m (1%) OTM put option (position seems good even if the underlying spot goes either sideways or spikes mildly), simultaneously, go long in 2 lots of delta long in 2m ATM -0.49 delta put options (spot reference: 134.250 levels while articulating).

The position is a spread with limited loss potential, but varying profit potential. The degree of profit relies on the strength and rapidity of price movement. The position uses long and short puts in a ratio, such as 2:1 or 3:2, to maximize returns. Courtesy: Sentry & JPM