U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

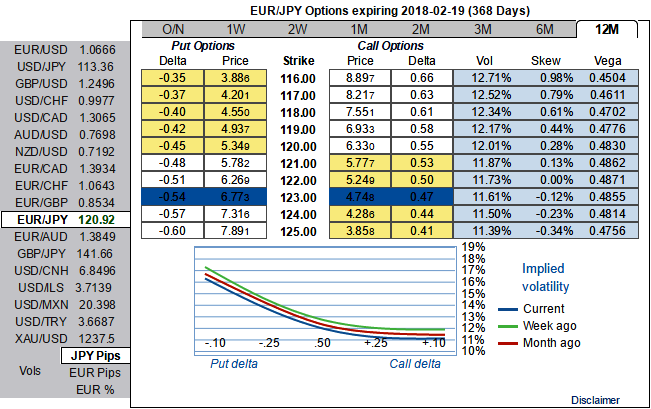

The EURJPY volatility surface is currently offering very attractive opportunities, as ATM volatility is rich and 6m/1y skews are excessively priced. Here, we recommend a couple of trades taking advantage of both the volatility and skew premiums.

In the volatility space, going short a 6m variance swap provides extremely high-profit odds. EURJPY 6m realized volatility has spent 78% and 89% of the time below the current variance swap bid level since 2007 and 2011 respectively.

We keep our EURJPY bullish bias as a directional reflation trade, which can be advantageously expressed via a zero-cost 3m topside seagull strikes 123.1715/121.1217/125.

Volatility trade: go short EURJPY 6m variance swap @14.3 (EUR indicative bid).

Trade risks: 6m realized volatility below 14.3 in 6m. Investors receive or pay the squared difference between the 14.3 strike and the terminal realized volatility and face unlimited losses if realized volatility is beyond this strike level.

Directional trades: Buy EURJPY 3m topside seagull strikes 123.1715/121.1217/125 Zero cost (indicative offer, spot ref: 120.9220).

Trade risks: unlimited below 123.1715. The structure is buying a standard call spread strikes 121.1217/125 fully financed by selling a put strike 123.1715. As such, investors face unlimited downside risk at the expiry if EURJPY trades below 123.1715.