Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance

BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions

Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

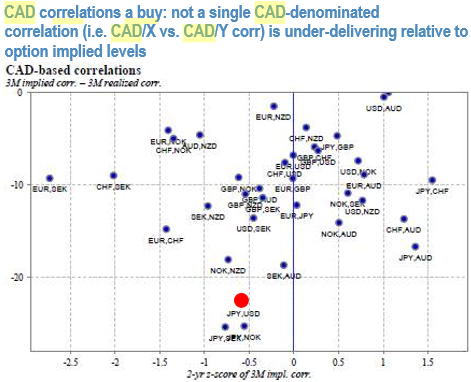

CAD-based implied correlations are priced well below realizeds for nearly the entire CAD-cross universe; owning CADUSD vs CADJPY corr. or a CADJPY - USDJPY vol spread is a positive carry NAFTA hedge. Notably, please be informed that the CAD implied vols are on lower side among G7 FX space.

As we have done with the Brexit-driven long GBP vol theme this year, NAFTA or BoC-related CAD-volatility is best isolated via easy-to-carry relative value structures. CAD-denominated correlations are a rich seam of trades to mine in this regard, as implied correlation in not a single CAD/X vs. CAD/Y pair is priced above trailing realizeds, and in most cases actually trades steeply under (refer above chart).

Among the relatively more liquid pairs, the most discounted CAD-corr of interest is CADUSD vs CADJPY (3M implied corr. 51, realized corrs 1-mo 75, 3-mo 73).

Given the low-yielding / funding currency status of both USD and JPY, and CAD’s traditionally tight link to the global growth cycle that tends to exert similar directional influence on both pairs, above-average correlation is the norm rather than the exception for CADUSD and CADJPY; chart 6 shows that a hypothetical strategy of systematically owning CADUSD vs CADJPY correlation swaps would have generated high Sharpe Ratio returns (excluding transaction costs, hence hypothetical) over a long history spanning multiple volatility cycles.

A transaction-cost friendly version of the full correlation triangle is to buy CADJPY – USDJPY vol spreads that are historically low (6M ATM spread 0.9 vs. 3-yr avg. 1.6), offers marginal (0.5 vol pts.) RV edge vs. the corr swap to go with greater liquidity, insulation to any idiosyncratic yen volatility stemming from an earlier/larger-than-expected re-set of the BoJ’s 10YY JGB yield target, and is similar in spirit to the GBPJPY – USDJPY vol spread we bought in the 2018 Outlook to hedge against any Brexit-related upheaval in the pound.

One concern is idiosyncratic USD volatility –especially a sharp rise in Treasury yields that sparks large scale USDJPY buying –that can potentially derail the short leg of the vol spread; our sense is that the steady-as-she-goes message from this week’s FOMC, thinner Republican Senate majority after the Alabama result that reduces odds of big bang fiscal (infrastructure) legislation, and seasonal softness of US data in 1Q renders that particular risk manageable through the first few months of next year. Courtesy: JPM