S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand

JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

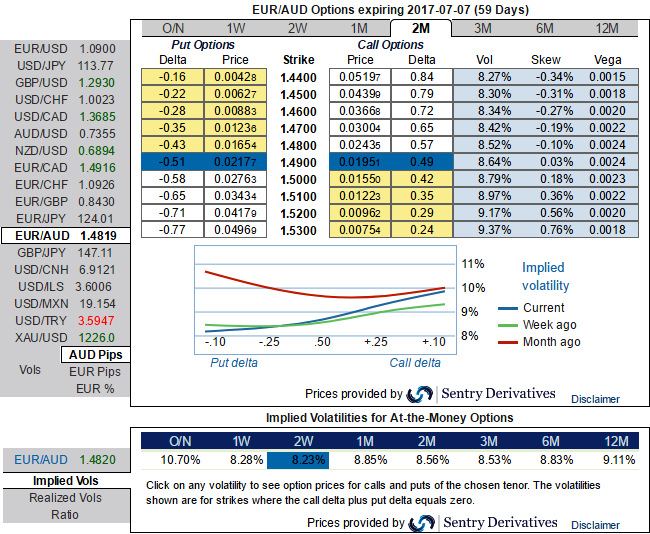

We’re adding EURAUD to boost our overall EUR exposure as the passage of the French election this weekend should clear the way for an intensification of portfolio inflows into the region in keeping with the cyclical acceleration in the region’s economy (the Italian election is too distant a prospect to command a risk premium).

AUD, by contrast, is likely to be weighed down, firstly by its stand-out sensitivity to China sentiment (underlying economic linkages and Australia’s status as a liquid proxy for China), and secondly by the downside risks to RBA policy in 2H17, including from a housing market that’s not liking its macro-prudential medicine.

There’s the risk of a tactical bounce in AUD from next week’s Federal budget (more infrastructure spending?), but this should be short-lived.

In the case of optionality, the 2m implied are projected to spike above the current realized (refer above nutshell).

Importantly, that the risk is essentially pricing in the bullish case, as it is linked to the possibility of volatile euro spikes. We articulate the euro’s technical trend against Aussie dollar in our recent post.

For more reading, please go through below weblink:

Thus, we like being short vol in short run, selling that premium conditionally on a pay-off benefiting from a lower spot.

Prefer a ladder to a call spread ratio As we expect limited spot appreciation and topside volatility, we recommend buying a 2m call ladder. Buy 1 ITM Call of 2m tenor, simultaneously stay short in 1m 1 ATM Call and Sell 1 OTM Call of positive thetas (strikes 1.4450/spot/1.5080).

That structure improves the odds compared to a call spread ratio as the maximum and constant profit zone is reached over a range instead of a single spot level.

However, risk is potentially unlimited above 1.5080, and investors would have to delta-hedge dynamically the trade in the event of fast upside.

Buy-and-hold structure and Greeks’ behavior: The above profile sells convexity. Being short gamma implies a buy-and-hold profile, as the full leverage can only be monetized at the expiry.

Finally, the short vega profile fits with the idea that a higher EURAUD should mean lower implied vol, consistent with the negative skew. Front-end risk reversals turned positive with the French election fetches as predicted results as Macron managed triumph (EURAUD has usually a positive skew).