BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

The Fed’s this month’s meeting decision is almost in lines of consensus. Do you think the shift in dynamics this time around is due to the improved growth prospects on account of tax changes and market’s expectations for fewer rate hikes next year?

While gold prices soared back to $1263.77 levels, yellow metal price has usually been sensitive to moves higher in both UST yields as well as the US dollar, the bullish dollar leads bullion market costlier for holders of foreign currency while a rise in U.S. rates, lift the opportunity cost of holding non-yielding assets such as bullion.

While we roll short to Feb’18 CME gold, short in gold since September 20 has been encouraged owing to the view that the market remained under-pricing Fed tightening, given solid economic growth and a possible bottoming out in inflation. Some repricing has already taken place.

In early September, the rate markets priced no hikes through 2018, during November just over two hikes (55 bps) were priced in. On Wednesday, Dec 13, the Fed elected to raise the Federal Funds Target rate by 25 bp to 1.25-1.50% while maintaining an outlook for three more hikes next year.

The JPM base case is that incoming Chair Powell will hike in March followed by three more hikes in 2018. As the market is currently pricing in around a 66% chance for a hike in March, we believe gold will continue to reprice lower over the next couple of months and stay short.

Originally went short Dec’17 CME gold at a price of $1,318/oz on September 20, 2017. Rolled to Feb’18 contract on December 14, 2017, embedding the roll gains into our entry level, which increases to $1,321.20/oz.

Trade target is $1,190/oz with a stop at $1,384/oz. Marked to market December 14, 2017, at $1,255.50/oz for gain of $65.70/oz or 5.0%.

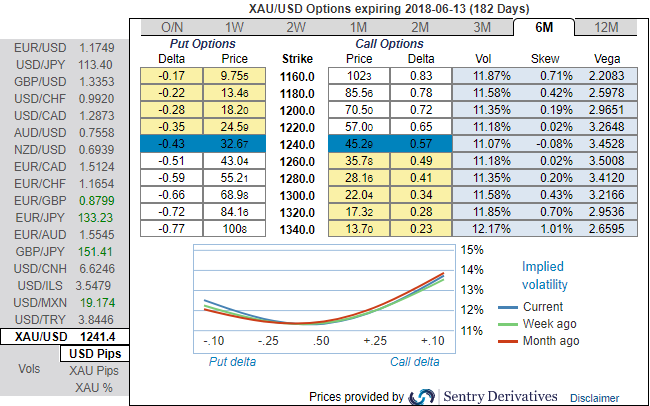

Alternatively, risk-averse traders who are dubious about upside move, go long in XAUUSD 3M at the money -0.49 delta put, and go long 6M at the money +0.51 delta call and simultaneously, Short 1m (1%) out of the money calls. Thereby, we favor bulls as we foresee more upside risks by keeping longer tenors on call leg.

For 6m IV skews have been well balanced and signify the hedgers’ interests on both OTM call and put strikes. While the combination of 1m bearish neutral remains intact with shrinking IVs is conducive to writing overpriced OTM calls. Using three-leg strategy would be a smart move to reduce hedging cost.

While it is reckoned that as per the OTC indications as shown above and the prevailing trend in bullion markets seem to be reasonably addressed by hedging participants, thus, we advocate below option strategy to keep uncertainty in spot gold prices on the check. On trading perspective also, the strategy likely to fetch positive cashflows regardless of underlying price swings with more potential on the downside and with cost-effectiveness.