Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

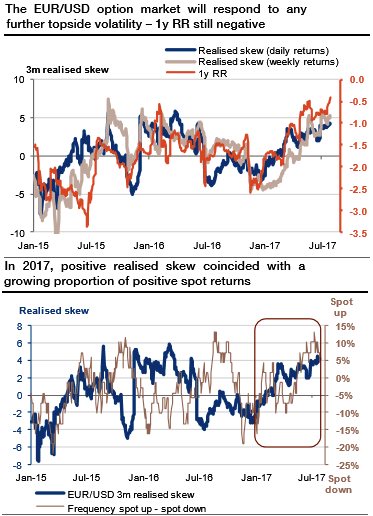

We’ve stated in our recent posts about euro positive skewness. But the options skew reflects the relative appetite for calls and puts, which only partly reflects pure directional expectations. The skew is primarily about volatility expectations conditional on a scenario on the spot. The sensitivity and focus on reassessing central bank policy, and the ongoing vulnerability of the dollar. The theme of Europe leading outperformance remains dominant; maintain core EUR or proxy longs as data continue to be supportive, but increase USD shorts.

Market makers essentially trade the skew as per their perception of topside compared with downside volatility. To this end, we computed a realized skew that can be used like realized volatility. Namely, we computed the spread between two exponentially weighted realized volatilities, based on positive and negative returns (refer above chart). Dollar weakness continues to preserve prevailing vol themes of gamma strength, curve flattening and risk-reversal softness.

When the realized skew is positive, it shows that the FX rate experiences more topside than downside volatility. As expected, this metric is strongly correlated to the risk reversal. One could argue that using daily returns only captures market nervousness or noise, instead of meaningful spot moves.

So we also computed the realized with weekly returns instead of daily returns, and observe that our realized skew is relatively insensitive to the returns frequency. If we zoom in on the recent period, the EURUSD daily realized skew switched to positive territory in early March, while the weekly realized skew made this move at end-April. This fits with the EURUSD break of 1.08 right after the first round of the French presidential election.

Societe Generale reckons that the options market should respond to further topside vol:

Even if it has not always been true, the rise in the realized skew observed in 2017 happened on the back of a growing proportion of EURUSD positive returns (refer above chart). If EURUSD vol rises from limbo as the spot overshoots upwards, risk reversals should exhibit more bullishness.

As we have emphasized, the ECB still has to clarify how the QE process will reverse. The 2015-17 EURUSD range corresponded to its asset purchase period, and, more globally, the negative skew period (since 2009) corresponded to global central banks’ accommodation. As the market is still awaiting the next steps from the ECB and Fed, the full positive impact on the EURUSD skew is probably yet to be seen.