Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

As anticipated, the RBA board meeting for interest rate decision, has not bring in any change, that the board has decided to hold the cash rate steady at 2.0%. With the market probability of a move near to zero, that is a sharp contrast to some months ago when markets gave a 100% probability to a rate cut by February.

We are bearish on this APAC pair after Aussie produced a lackluster trade balance numbers at negative 3.54M to miss the forecasts at 2.50M and a slump from previous flash at 2.727M. While exports have been highly disappointing steep slumps from previous -1% to -5% and imports were unchanged at -1%.

On the flip side, BoJ's negative rates that keeps JPY back in action. Technically, after the event we've been observing consistent recovery in JPY against Aussie dollar, the pair has breached a support 85.646, we think the pair has gone fragile to evidence more dips upto next strong supports at around 83.400 and 82.914 and on intraday terms now again failed to hold the crucial supports at 83.947 levels and slid below 21DMA, as a result more weakness is anticipated in this pair at current level.

By pushing rates into negative territory, the BOJ is in effect penalizing commercial banks for not lending aggressively by charging the institutions for holding excessive reserves at the central bank.

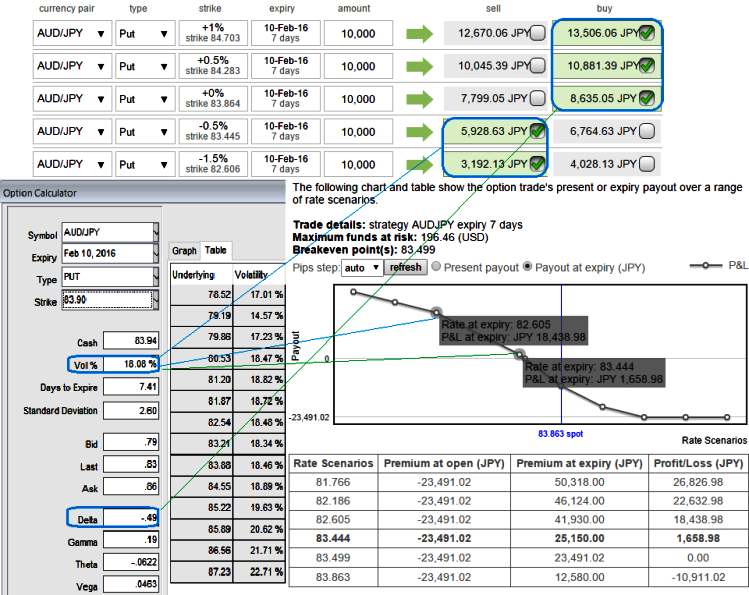

The implied volatility of 1W ATM AUDJPY put contract has increased a bit, it is now more than 18% which is quite on higher side that is good sign for option writers.

We reckon that the contracts with spiking IVs cost more, intuitively due to the higher probabilities of the market 'swinging' in as per the research. If IV increases and you are holding an option, this is good. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

Hence, as shown in the diagram weights have been doubled and resulted into huge cash inflows for every small change in underlying exchange rate.

As we expect the underlying currency exchange rate of AUDJPY to make a larger move on the downside. As shown in the figure go long in 3 lots of different striking put options and simultaneously short 4D (0.5%) in the money put option and one more 1W (1%) in the money put options (choose both short sides that should have positive theta and delta closer to zero).

Long side, 2W at the money -0.52 delta puts, 3W (0.5%) out of the money -0.21 delta put and 1M (1%) deep out of the money -0.16 delta put options are recommended. The strategy would be constructed for net debit, narrow expiries are the most essential to ensure the short side expire worthless.

Entering into this AUDJPY position which has higher implied volatility at 18% and expecting for the inevitable adjustment is a smart approach, regardless of the direction of price movement.

Based on volatility and time decay, the strategy is a "price neutral" approach to options, and one that makes a lot of sense.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: AUD/JPY put writers on upper hand on higher IVs and interim rallies – 3:2 PRBS for both hedging and speculating

Wednesday, February 3, 2016 6:45 AM UTC

Editor's Picks

- Market Data

Most Popular

7