Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  God on their side: how the US, Israel and Iran are all using religion to garner support

God on their side: how the US, Israel and Iran are all using religion to garner support  Time to buy local: war fuel price shocks reveal the folly of a long food supply chain

Time to buy local: war fuel price shocks reveal the folly of a long food supply chain  How the war in Iran is already affecting UK farmers and food production

How the war in Iran is already affecting UK farmers and food production  Makemation: a Nollywood movie that shows AI in action in Africa

Makemation: a Nollywood movie that shows AI in action in Africa  Gold is meant to be a ‘safe haven’ in uncertain times. Why is it crashing amid a war?

Gold is meant to be a ‘safe haven’ in uncertain times. Why is it crashing amid a war?  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

The FX volatility is very low and turnover suggests that participation is also declining. This is highlighted by the tight ranges in FX despite substantial reversals in both equities and debt markets. We reckon the stasis in the FX market is symptomatic of a market approaching a pivot point.

Dual changes are likely, the first one is that the dollar, which has been the dominant driver could be giving way to risk appetite again, as the market throws in the towel on its weaker USD views yet again. With risk appetite in other markets ‘euphoric’, this tilt could well drive a substantial rise in FX volatility.

The latter potential change is that the FX market may drift away from trading in a top-down fashion. As divergences appear between both the outlook for growth in economies and the reaction function of central banks, we think a bottom-up approach to the market could become the path to success.

As the bearish trend in FX volatilities continues, the appeal of buying optionality at low entry levels clashes with the negative time decay options suffer when catalysts for higher realized vols are missing.

We try to shed some light on the perennial debate between tactical vs strategic vol investment approaches by updating a systematic FX short-vol trading model introduced in March. As we write, the model would largely keep the short-vol bias.

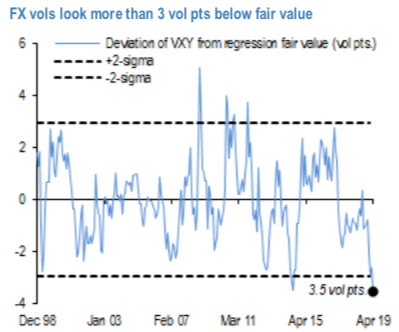

Despite the rebound as occurred during the last week of April, FX vols remain near historical lows. Current volatility levels appear more than 2 std.devtn. undervalued based on the J.P. Morgan cyclical fair value for FX vols (refer above chart). In this market characterized by ultra-depressed volatility levels, the strategic appeal of holding long-optionality positions clashes with the multi-month trend dragging vols even lower, thus impacting long positions via time decay.

In the first part of this note, we update a systematic FX short-vol model as released earlier this year, for shedding some light on the perennial debate between tactical vs strategic approaches when managing vol trades.

Also, it appears natural to look for possible catalysts towards higher FX vol levels by investigating relationships involving other asset classes, as done for instance in the J.P. Morgan View, the rolling bear market in volatility. In the second part of the note, we focus on the possible relationship between FX and rates vols. Courtesy: ANZ & JPM

Currency Strength Index: FxWirePro's hourly EUR spot index is inching towards 77 levels (which is bullish), USD is at -8 (neutral), while articulating (at 08:23 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex