Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

There is a late swing in the Italian opinion polls in favour of MS5. While holding forecasts unchanged, we have established a decent long EUR position in the macro portfolio (vs JPY, NZD, and an EURUSD proxy).

The concerns about the Italian elections mount in 1Q’18 that poses bullish risks to the Swiss franc. While the election frontrunner Matteo Salvini said his party is ready to withdraw from the European Union and the Eurozone unless Brussels stops "victimizing" Italy with harsh economic demands.

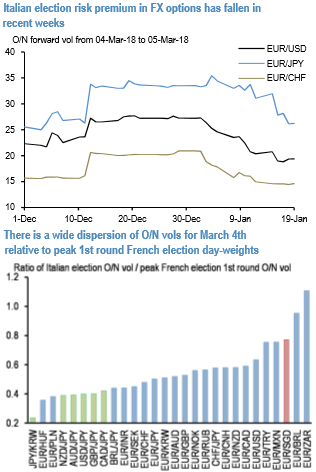

Italian election risk premia have continued to slide this year (refer above diagram), and yen-crosses, in particular, have been the largest casualties of the re-pricing.

At current levels, 4th March O/N vol levels in JPYKRW (8.7), AUDJPY (14.2), USDJPY (11.1), GBPJPY (13.7) and CADJPY (13.7) all look unthreatening, especially when compared to the frenzy of the French election episode (refer above diagram).

On average, options markets are priced at 50% of the event premium of the 1st round of the French vote from last year which is perhaps fair on the whole, but there is significant dispersion across currencies that creates the potential for relative value:

JPY crosses are at the cheap end of the spectrum with an average French election O/N multiple of 0.4.