FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

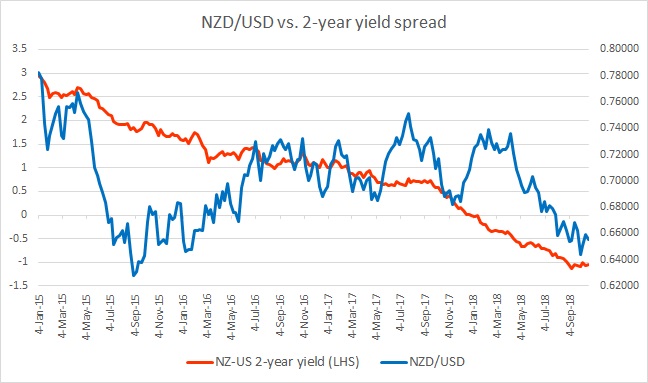

The chart above shows, how the relationship between NZD/USD and 2-year yield divergence has unfolded since 2015.

While the spread has narrowed steadily from +300 basis points (bps) in January 2015 to -106 bps as of September 2018, the New Zealand dollar has been pretty volatile around the spread. However, from the chart, it’s quite clear that the direction of the spread is playing a crucial role over the medium to long-term.

We have forecasted a lower NZD against the USD with a target of 0.59 against the USD over the medium to long-term, and with the Reserve Bank of New Zealand (RBNZ) continuing its dovish rhetoric, we expect the spread to decline further in favor of the USD.

In October, the spread has further declined by 3 bps to - 105 bps and the New Zealand dollar declined from 0.668 against the USD to 0.655 against the USD. If the spread halts decline, it would be of extreme importance as it taking place near a crucial support of 0.65 area.