ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  Asian Currencies Steady as Trump-Xi Summit, Inflation Concerns Boost Dollar

Asian Currencies Steady as Trump-Xi Summit, Inflation Concerns Boost Dollar  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects  South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge  Gold Prices Steady Ahead of Trump-Xi Meeting as Inflation and Oil Concerns Persist

Gold Prices Steady Ahead of Trump-Xi Meeting as Inflation and Oil Concerns Persist  Oil Prices Hold Above $100 as Trump-Xi Meeting and Iran Conflict Keep Markets on Edge

Oil Prices Hold Above $100 as Trump-Xi Meeting and Iran Conflict Keep Markets on Edge  Trump Pushes China Market Access During High-Stakes Xi Summit

Trump Pushes China Market Access During High-Stakes Xi Summit

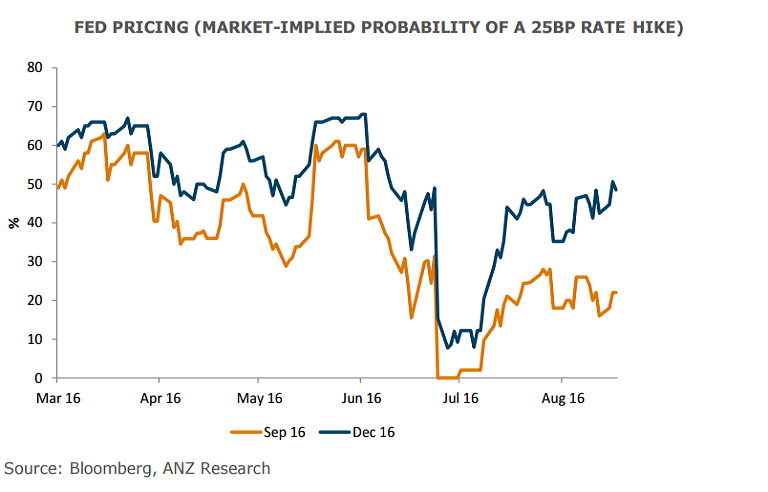

US Federal Open Market Committee minutes released overnight highlight that officials are divided, with no clear indication of when the central bank will hike next. The minutes showed that members were generally upbeat about the economic outlook and labor market, but several said a slowdown in the future pace of hiring would argue against a near-term hike. The market currently is 22 percent priced for a move in September and just under 50 percent for December.

Fed officials have recently reminded the market not to be too complacent and that the bias at the Fed is still to raise interest rates. NY Fed president Dudley’s said on Tuesday that markets are too complacent about rate hike risks. Dudley said he expected stronger growth in the US in H2 than in H1 and further improvement in the labour market. That sentiment was echoed by FRB Atlanta President Lockhart.

“Hawks balanced with doves and the Fed in wait-and-see mode,” said Kit Juckes, strategist at Societe Generale. “I don’t think this tells us much about the September meeting, which is, as ever, data- and market-dependant, but it does tell us that the most we’ll get is a very slow and cautious tightening path.”

The key to when the central bank moves remains the underlying data flow. Recent data suggest growth probably accelerated in Q3. Headline Q2 GDP growth (+1.2 percent saar) was disappointing, but underlying activity was still positive and will remain supported by stimulatory financial conditions. Residential investment, which was a significant drag on Q2 GDP appears to be recovering. Recent solid gains in employment suggest underlying momentum is better than the headline GDP.

That said, despite signs of a pickup in wage growth, headline inflation remains below target. July CPI fell to 0.8 percent y/y from 1.0 percent in June and the PCE is hovering at 0.9 percent y/y. Core inflation is closer to the Fed’s 2 percent target. University of Michigan 5-10yr inflation expectation remains low but stable at 2.6 in July.

"An ongoing tightening in the labour market and relatively stable inflation expectations point to a gradual return in headline (PCE) inflation towards the target (2 percent) over the near to medium term," said ANZ in a report to its clients.

The FOMC's next meet (21-22 Sept) will be accompanied by a press conference from Janet Yellen and the updated Summary of Economic projections (including the fed fund rate). Hurdle probably remains a little high for September rate move. Another round of monthly data (employment and CPI) will be available for scrutiny. However, one month of data may not be sufficient to provide the confidence the Fed needs.

The dollar saw choppy trading, shorter-term Treasury prices turned higher and stocks nudged into positive territory after the release of minutes on Wednesday. DXY extending dips on the day, down 0.36 percent at 94.39 at 11:30 GMT. USD/JPY was at 100.19 while EUR/USD was at 1.1327.