Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns

Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns  South Korean Stocks Tumble as AI Chip Selloff Hits Asian Markets

South Korean Stocks Tumble as AI Chip Selloff Hits Asian Markets  Asian Currencies Stay Under Pressure as Dollar Holds Near 13-Month High Ahead of U.S. Jobs Report

Asian Currencies Stay Under Pressure as Dollar Holds Near 13-Month High Ahead of U.S. Jobs Report  Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes

Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  New Zealand Consumer Confidence Rises in June as Inflation Expectations Ease

New Zealand Consumer Confidence Rises in June as Inflation Expectations Ease  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Moody’s Says Peru’s President-Elect Keiko Fujimori Could Boost Investor Confidence

Moody’s Says Peru’s President-Elect Keiko Fujimori Could Boost Investor Confidence  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions

Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions  U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk

U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

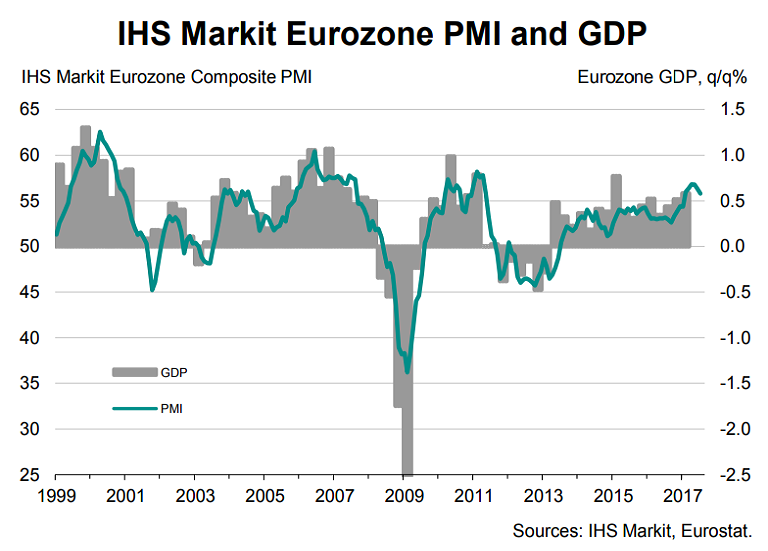

IHS Markit's euro zone Flash Composite Purchasing Managers' Index for July fell to 55.8 from 56.3 in the previous month. The reading was below median expectation in a Reuters poll for a modest dip to 56.2. Despite coming off recent highs, the composite PMI index was still comfortably above the 50 level that separates growth from contraction and suggested that Euro zone businesses started the second half of 2017 with solid growth.

The upturn was once again broad-based. Manufacturers continued to report stronger output growth than service providers, despite the rate of expansion easing to the weakest since January. The rate of job creation continued to run at one of the highest seen over the past decade. Forward-looking indicators such as new order inflows remain elevated, suggesting robust growth will continue into coming months.

"It still looks like a robust, broad-based sustainable upturn, it's just losing a bit of momentum and it's too early to get too worried about this. The PMI, if maintained, pointed to third quarter GDP growth of 0.6 percent," said Chris Williamson, chief business economist at IHS Markit.

Meanwhile, the European Central Bank’s announcement of not cutting interest rate any further might be construed as a baby step towards normalisation despite continuing stimulus spending through its trillion Euro bond buying activity. Years of ultra-easy policy may be bolstering growth, but the central bank is struggling to bring inflation to target range and will likely be in no rush to taper policy.

That said, the economic situation in the eurozone continues to improve and the risks are balanced. Following ECB President Mario Draghi’s speech at Sintra in late June, the markets saw a strong adjustment. The 10y Bund yield rose more than 30bp. The September meeting is still critical and markets will look for change in the wording of the forward guidance. The ECB is also set to presents new staff projections at its September meeting.

Patrick Jacq, Research Analyst at BNP Paribas suggests that the ECB will be more vocal in September as there was no significant change in ECB rhetoric at its final press conference on 20 July before the summer rest period.

EUR/USD has been on an uptrend since Jan 2017. The pair has risen almost 13 percent since the beginning of the year. Today, EUR/USD was down 0.11 percent, easing from fresh 11-month highs at 1.1684. The pair finds stiff resistance at weekly 200-SMA at 1.1794. Break above could see breakout of major channel top and test of 1.25 levels then likely.

FxWirePro launches Absolute Return Managed Program. For more details, visit http://www.fxwirepro.com/invest