US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms

US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms  US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus

US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy  Asian Currencies Stay Under Pressure as Dollar Holds Near 13-Month High Ahead of U.S. Jobs Report

Asian Currencies Stay Under Pressure as Dollar Holds Near 13-Month High Ahead of U.S. Jobs Report  Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions

Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Trade surplus in excess of USD 1bn used to prompt cheers in the markets but this was not the case for July's USD 1.3bn. Perhaps markets are no longer concerned about the current account (C/A) deficit, which has indeed narrowed to a sustainable 2% of GDP in 1H15. More importantly though, markets seem to have fully understood that poor import growth (and not strong export growth) has been driving Indonesia's trade surplus so far this year.

The holiday distortions mean that we can't just single out the July trade data. Still, for the year-to-date, imports are down by close to 20%. It is not simply due to currency valuation as the rupiah has lost about 10% of its value against the dollars. Slower underlying demand must have explained the other 10%-pt fall in imports this year.

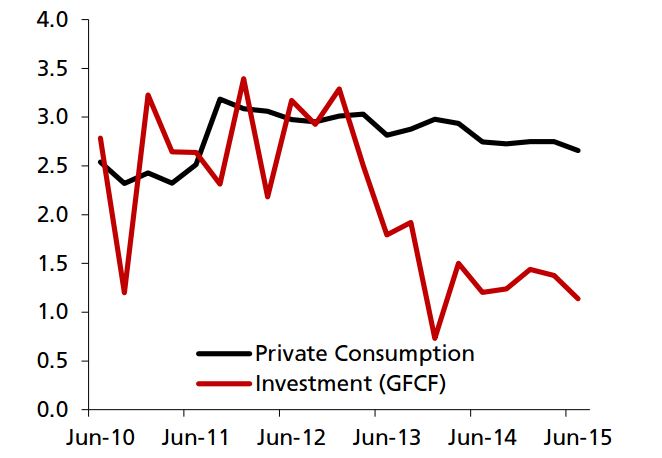

Investment growth is the biggest drag to overall GDP growth this year. A lot has been said about the moderation in consumption but consumption growth is still trending a decent 5%. It is investment growth that has been disappointing in 1H15 and the government was partly to blame. Up until mid-July, disbursement of capital expenditure was only about 15% of the full-year's target. Given the poor sentiment in the private sector, the economy needs this acceleration in public investment to provide the much-needed support.

Until there are signs that export growth has turned the corner, a wider trade surplus may only mean a further slump in domestic demand. And this is a worrying sign at a time when there are plenty of downside risks to GDP growth.