FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

RBC Capital Markets notes:

1 - 3 Month Outlook - New lows in prospect

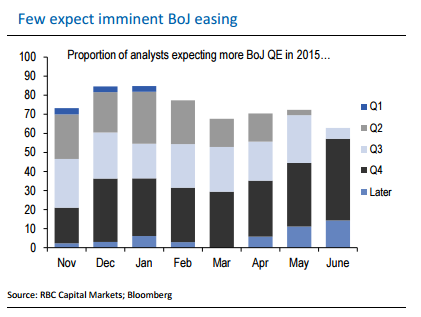

USD/JPY lurched up to a new 13 year high (125.87) in earlyJune, but another string of comments from MoF and BoJ officials suggesting little scope for further JPY weakness capped the move and the last couple of weeks have seen consolidation in a 122-124 range. We expect USD/JPY to make more new highs in Q3 and JPY's apparent loss of safe-haven status removes another obstacle to this happening.

In the latest three months there were no JPYcrosses significantly correlated to equity returns except CHF/JPY and in that case, JPY is trading as the risky asset and CHF the safe haven. This is unprecedented in the postcrisis era when typically (85% of the time) all JPY crosses with the exception of USD/JPY have traded as proxies for general risk appetite, with JPY as the safe haven. This remained true right up to the early months of this year . That JPY's apparent loss of safe-haven status is such a recent phenomenon has to leave a question mark over how sustainable it is, but for now that JPY appears to benefit much less than it did in periods of risk aversion removes another obstacle to near-term USD/JPY gains. That JPY's status is changing should perhaps not be that surprising.

Japan's external flows have undergone a transformation in recent months due to the reallocation of public sector assets overseas, which at the very least should be neutralising some of the flow that was at the root of JPY's safe haven status. These sustained (and unhedged) equity outflows are also a key reason why we are bearish JPY near-term.

6 - 12 Month Outlook - Waiting for the final seller

These domestic public sector flows drove the move from 100 to the 120s. Prior to that, the overseas sector fuelled the move from 80 to 100. The sector we expect to drive the third leg of JPY selling has so far had limited involvement and appears to be largely indifferent to domestic policy - the Japanese private sector, specifically, bond investors. Unlike equity flows, the raw bond flows tell us little about the supply/demand balance for the currency as much fixed income investment is currency hedged.

Indeed for fixed income investors, shifts in hedging behavior have the potential to generate much bigger FX flows than the crossborder asset movements themselves as they affect the entire stock of existing investment, not just the current flow. As US short rates rise, so does the cost of hedging and we still expect an unintended consequence of higher US rates to be another big leg down in JPY (target: 132).

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Currency Outlook: Japanese Yen

Tuesday, July 7, 2015 12:18 AM UTC

Editor's Picks

- Market Data

Most Popular