RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  UN Chief Urges Nations to Close $100 Million UNRWA Funding Gap

UN Chief Urges Nations to Close $100 Million UNRWA Funding Gap  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  US Stock Futures Steady as Investors Await Payrolls Data and Monitor Iran Tensions

US Stock Futures Steady as Investors Await Payrolls Data and Monitor Iran Tensions  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  NATO Albania Summit Faces Uncertainty as Trump, Defense Spending Concerns Loom

NATO Albania Summit Faces Uncertainty as Trump, Defense Spending Concerns Loom  India Manufacturing PMI Slows in June as Demand Weakens Despite Lower Cost Pressures

India Manufacturing PMI Slows in June as Demand Weakens Despite Lower Cost Pressures

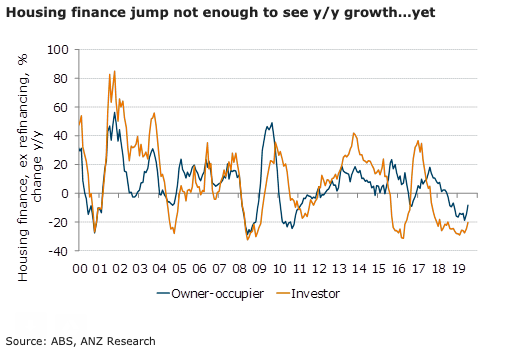

Australia’s demand for mortgages picked up sharply in response to rate cuts in June and July, with 5.1 percent m/m growth in July. The strength was reflected across both owner-occupiers and investors. The Reserve Bank of Australia (RBA) is unlikely to be impressed by these numbers, according to the latest report from ANZ Research.

Investor lending was up 4.7 percent m/m in July, ex-refinancing, the strongest monthly result since September 2016. This is a strong sign of investor optimism after sharp declines in investor demand during the housing price adjustment. Annual growth in investor lending is still sharply negative (-20.4 percent y/y to July), however this is the smallest negative result since July 2018.

Owner-occupier lending grew 5.3 percent m/m in July ex refinancing, the highest result since August 2015. Annual growth is still negative (-8.3 percent y/y), but it is the smallest negative result since October 2018.

Interestingly, approvals for the purchase of new homes jumped 20.8 percent, the strongest rise since 2001. This suggests that the pick-up in housing prices and finance will soon feed through into construction activity.

Regulatory easing in July (APRA relaxed the 7 percent+ floors on mortgage serviceability) heightened the effects of rate cuts, by allowing lower rates to more directly affect serviceability assessments.

Optimism in the housing market following green shoots in prices in Sydney and Melbourne prices may have also spurred on extra demand. Ongoing elevated auction clearance rates suggest that the strength has continued into September.