Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence

Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence

Last night’s FOMC minutes for September did little to change the market’s expectations for upcoming policy meetings.

The implied probability of a 25bp hike from the Fed in November and December remain close to 20% and 70% respectively.

Our base case remains for a hike in December.

Today’s BoE governor Carney’s speech would be factored in rate cut hopes if UK construction figures for August presents the final piece of official ‘hard’ output data in advance of the preliminary estimate of Q3 GDP.

Based on the flow of relevant data as a whole, our bean count so far suggests Q3 GDP growth of 0.4% QoQ, well ahead of the BoE’s assumptions from the August Inflation Report.

Meanwhile, US September retail sales are likely to retrace some of the softness last month, helped by strong car sales. We look for a rise of 0.6% in line with the market consensus. Preliminary US October consumer sentiment is expected to rise for the second month.

For today, the market focus would fall on appearances from BoE Governor Carney and Fed Chair Yellen’s speech.

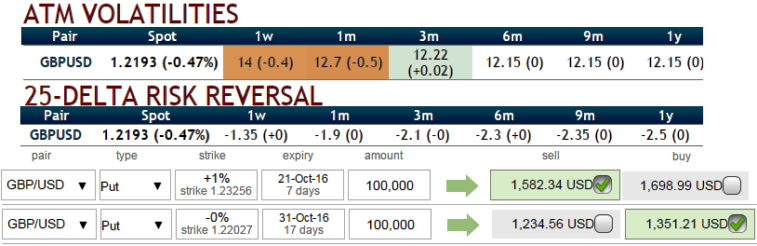

OTC Outlook and FX Option Strategy:

The rationale: Use upswings to deploy “credit put spreads” as the chances of the retest of recent lows of 1.2089 is quite a possible event.

Upside potential is limited in the short run as you can see bullish neutral risk reversals in 1w expiry with negative sentiments in OTC over long-term tenors and this should be cushioned & used for shorts during reducing volatility times.

The 1w ATM implied volatility is up about 14% and likely to perceive at 12.7% in 1m tenors.

Well, any abrupt upswings should not be panicky, instead deploy them in the below option strategy.

Execution: Keeping risk reversal, IV and trend factors in mind, it is advisable to go long in 1m ATM -0.49 delta put while writing 1W (1%) ITM put with positive theta and delta closer to zero (both sides use European style options).

Add longs to favor major downtrend, dips should optimally be utilized so as to participate in that major trend, while deploying ITM short puts capitalizing short-term upswings. Thereby, the profitability can be maximized for every shift towards downside and this is not the same on the upside.