JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?

Slowdown in Chinese economy has created havoc for commodities across world and its producers.

Naturally a though has occurred -

After two years of sharp slowdown and currency market adjustment, question arises hasn't the market priced in China weakness already.

- What I mean is, Chinese economy has slowed down to 7% from double digit growth just few years back and it is expected to continue to slow down in the foreseeable future.

- Given such fundamentals, Commodities have fallen sharply, say energy for which price has fallen close to 60% from its peak in 2014.

- Currencies both across emerging markets as well as developed market have adjusted significantly over this concern, for example New Zealand Dollar is down close to 19% this year so far, while South African Rand is down close to 28% in past one year.

So how likely is further devaluation both in commodities and currencies, which are dependent on China?

Very much...if China slows down further and sharply.

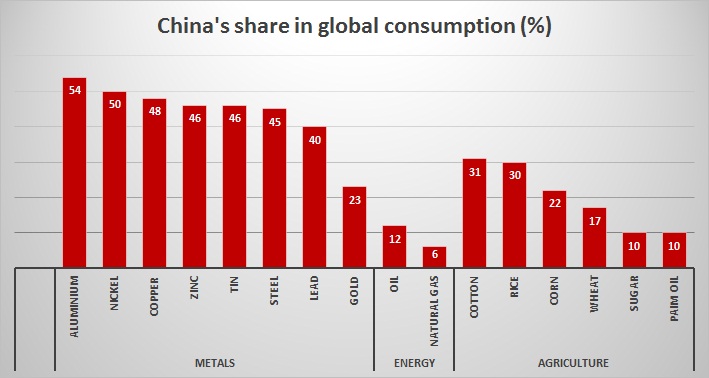

Because when it comes to commodities, China is still the glutton.

As of 2014,

Metals -

- China is consuming significant portion of world production of Aluminium (54%), Nickel (50%), Copper (48%), Zinc (46%), Tin (46%), Steel (45%), Lead (40%), and Gold (23%).

Energy -

- China is still not the largest consumer of energy products but raising consumption in both oil (12%) and natural gas (6%).

Agriculture -

- Not as large as industrials, nevertheless significantly large enough in Cotton (31%), Rice (30%), Corn (22%), Wheat (17%), Sugar (10%), and Palm oil (10%).