Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

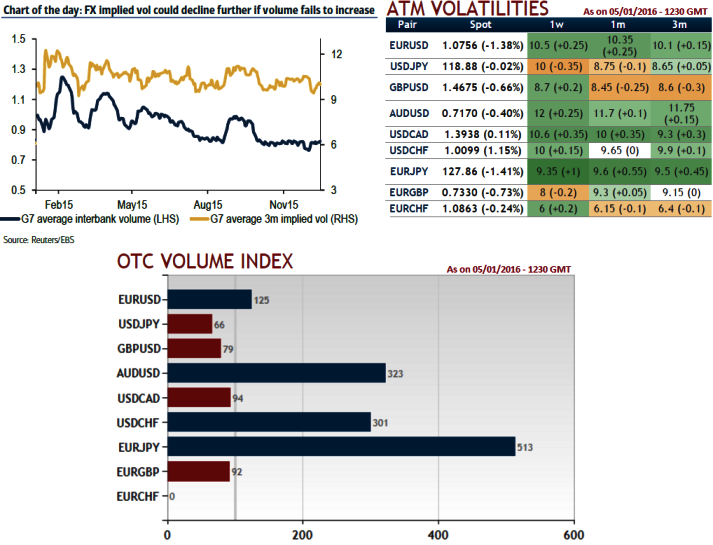

The FX volumes will have close correlation with macroeconomic theme that in turn will have impact on OTC markets.

We think there is vital aspect between RORO and FX volumes, when Risk-on & Risk-off illustrates investing a process, where investors move to riskier potentially higher yielding investments and then back again to supposedly lower yielding investments that are perceived to have lower risk.

Risk-on risk-off refers to changes in investment activity in response to global economic patterns.

For an instance, as shown in the diagram G7 FX interbank volumes spiked dramatically in late 2014 as central bank divergence themes gained traction (see circled area in the diagram). Similarly, options implied volatility rallied from multi-year lows.

In case of AUDUSD and GBPUSD pairs, observe the OTC volumes and IVs, there exists no disparity absolutely. Values on these liquid contracts over 100 indicate higher than average scenario that in turn influences implied volatility.

In our view, IV curve follows spot fx curve as there is growing expectation in OTC markets when underlying volumes starts accumulating and it is quite reasonable also, positive correlation between spot volume and options volatility for two main reasons.

First, both tend to increase when a fundamental story drives investor participation.

Second, rising volume creates sustained realized volatility, thereby justifying higher option premium.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Spot FX volumes directly correlate with implied volatilities in 2015, likely to continue in 2016

Wednesday, January 6, 2016 1:25 PM UTC

Editor's Picks

- Market Data

Most Popular