US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

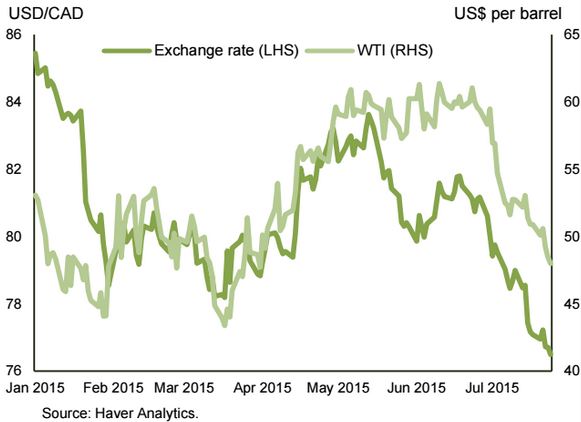

A variety of factors conspired to take the price of WTI below US$50 per barrel this week for the first time since March. When combined with last week’s Bank of Canada interest rate cut, this pushed the loonie under 77 US cents for the first time in over a decade.

Helping to round out some of the details on May’s economic performance, retail and wholesale trade data have reinforced our view that real GDP will be essentially flat in the month.

Add it all up and we are tracking a second quarterly contraction in real GDP in Q2 of roughly 1.0% (annualized). Looking beyond Q2, the lower Canadian dollar and interest rates should be supportive of growth, although the continued weakness in oil prices may delay renewed investment in the energy sector.

But looking beyond the second quarter, the lower Canadian dollar and lower interest rates bode well for Canadian exporters and manufacturers. Consumers should also to benefit. However, if current trends in commodity prices continue, business investment, particularly in the energy sector, may be slow to ramp up. The housing sector is likely to remain a bright spot in 2015, but can be expected to cool next year as affordability continues to erode on the back of national home price growth that is outpacing income growth. And with 5-year Government of Canada bond yields at around 80 bps, it’s hard to imagine rates going much lower.