RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

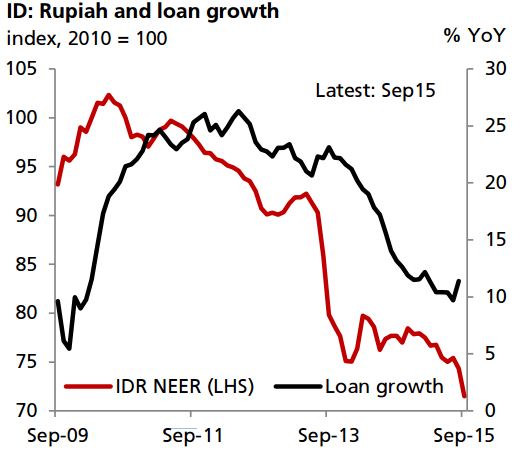

CPI inflation eased to 6.3% (YoY) in October and may fall further towards the year-end, given the high base effects from 4Q14. Note that monthly inflation is negative for the second consecutive month. Bank Indonesia (BI) cut interest rates in February, following two consecutive months of negative inflation. This time around, expectations are rising that BI may loosen its policy stance again, particularly following dovish signals from the October policy meeting.

That GDP growth remains lackluster is presumably a strong reason why some in the markets anticipate a rate cut. Yet, if underlying demand in the economy is weak, a rate cut may not boost loan growth by much at this juncture. The effectiveness of a rate cut in boosting GDP growth is questionable if businesses are not willing to make new investments anyway.

Confidence among business owners has taken a toll alongside the weaker rupiah in recent years. Arguably then, sentiment may not improve until we see some stabilization of the rupiah going forward. This is the main reason why BI has been active in the market to prevent excessive weakening of the rupiah. And it also explains why the central bank is no longer tolerant of a weak currency.

Uncertainties in global markets persist. Monetary policy divergences in the G3 economies are likely to keep the broad USD strength intact (see "Monetary policy divergences intact", 2 November 2015). An interest rate cut may send the wrong signals at this juncture. Despite BI's slightly dovish statement in October, a rate cut is not necessarily in the offing.