New Zealand Consumer Confidence Rises in June as Inflation Expectations Ease

New Zealand Consumer Confidence Rises in June as Inflation Expectations Ease  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears

Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations

Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations  Asian Currencies Rise as Dollar Weakens; Yen Holds Steady Amid Japan Intervention Watch

Asian Currencies Rise as Dollar Weakens; Yen Holds Steady Amid Japan Intervention Watch  China Services PMI Beats Forecasts as Strong Demand Supports June Growth

China Services PMI Beats Forecasts as Strong Demand Supports June Growth  Iran Begins Oil Sale Talks With Japan Under U.S. Sanctions Waiver Amid Shipping Risks

Iran Begins Oil Sale Talks With Japan Under U.S. Sanctions Waiver Amid Shipping Risks  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  US Resumes Dollar Shipments to Iraq After Months-Long Suspension

US Resumes Dollar Shipments to Iraq After Months-Long Suspension  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

Turkey’s cabinet decided to propose a State of Emergency (SoE) after a recommendation from the State Security Council yesterday. The state of emergency allows President Erdogan to rule by decree for three months, limit freedom of press and other constitutional liberties, and grants provincial governors extraordinary powers.

Turkey's average sovereign rating is at the risk of slipping to junk for the first time in three years. Moody’s rating agency on Monday this week placed Turkey’s Baa3 credit rating on review for a possible downgrade. Fitch Ratings also noted on Monday that there are ‘political risks’ to Turkey’s credit profile but didn’t take any ratings action. Fitch said its next scheduled sovereign rating review on Turkey is due on August 19th. Ratings agency S&P on Wednesday downgraded Turkey's sovereign credit rating.

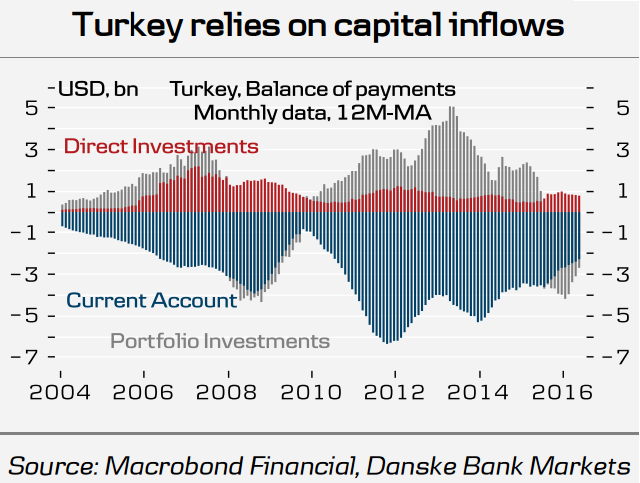

Positioning in Turkey has been reduced compared with early 2013 and its recent increased political predictability could see emerging market investors shift further out of Turkey. Although foreign investment increased 36 percent y/y in 2015 to US$16.5 billion (UNCTAD), figures for this year will be less impressive and far below the high water mark of $22 billion registered in 2007. Turkey still runs a relatively large current account deficit of around 4% of GDP and hence is in need of capital inflows.

The indebtedness of the non-financial corporate sector, which, according to the Institute of International Finance amounted to 56.8 percent of gross domestic product at the end of 2015, is low compared to developed markets, but it has risen substantially over the years. The rate at which this debt has expanded is second only to China and Turkey's companies are struggling to generate sufficient foreign currency to pay their dues.

S&P estimated Turkey must roll over just under half of its total external debt -- which it put at around $170 billion -- over the next 12 months. Turkey’s political landscape has fragmented further following the failed coup attempt, which will undermine the country’s investment environment, growth and capital inflows. Hence, the risk to Turkey’s ability to roll over its external debt has increased.

"In light of the changed political landscape in Turkey, we have lifted our USD/TRY forecasts to 3.12 in 1M (from 2.95), 3.20 in 3M (2.98), 3.25 in 6M (3.03) and 3.35 in 12M (3.05)," said Danske Bank in a report.

The Turkish lira has weakened around 6% since the attempted coup last Friday. Lingering political uncertainty is likely to weigh on capital inflows into Turkey and thereby on the TRY. USD/TRY was trading 3.0745 at 1045 GMT.