AstraZeneca Q2 Earnings Beat Forecasts as Oncology Growth Supports 2026 Outlook

AstraZeneca Q2 Earnings Beat Forecasts as Oncology Growth Supports 2026 Outlook  Domino’s Weighs Appeal After Australian Court Rules Workers Were Misled on Pay

Domino’s Weighs Appeal After Australian Court Rules Workers Were Misled on Pay  DOJ Subpoenas New York Times Freelancer Over North Korea Military Report

DOJ Subpoenas New York Times Freelancer Over North Korea Military Report  Johnson & Johnson Proposes $5.5 Billion Talc Settlement to Resolve U.S. Ovarian Cancer Lawsuits

Johnson & Johnson Proposes $5.5 Billion Talc Settlement to Resolve U.S. Ovarian Cancer Lawsuits  Eli Lilly Eyes AtaiBeckley Acquisition to Expand Psychedelic Mental Health Pipeline

Eli Lilly Eyes AtaiBeckley Acquisition to Expand Psychedelic Mental Health Pipeline  Takeda Hit With $885M Verdict Over Amitiza Generic Drug Delay Scheme

Takeda Hit With $885M Verdict Over Amitiza Generic Drug Delay Scheme  Brazil Supreme Court Approves Probe Into Lula’s Son Over Health Ministry Lobbying Claims

Brazil Supreme Court Approves Probe Into Lula’s Son Over Health Ministry Lobbying Claims  U.S. Unseals Charges Against Five Alleged CJNG Leaders, Raises Reward for New Cartel Chief

U.S. Unseals Charges Against Five Alleged CJNG Leaders, Raises Reward for New Cartel Chief  Maduro, U.S. Prosecutors Propose June 2027 Trial Date in Drug Trafficking Case

Maduro, U.S. Prosecutors Propose June 2027 Trial Date in Drug Trafficking Case  Warner Bros. Discovery Shares Rise as Newsom Pushes Settlement in $110 Billion Merger Fight

Warner Bros. Discovery Shares Rise as Newsom Pushes Settlement in $110 Billion Merger Fight  RFK Jr. Orders Extended Hantavirus Quarantine for Cruise Passenger

RFK Jr. Orders Extended Hantavirus Quarantine for Cruise Passenger  Brazil Supreme Court Tightens Jair Bolsonaro House Arrest Ahead of Election

Brazil Supreme Court Tightens Jair Bolsonaro House Arrest Ahead of Election  Trump Election Order Blocked Again as Appeals Court Rejects Mail-In Voting Push in 23 States

Trump Election Order Blocked Again as Appeals Court Rejects Mail-In Voting Push in 23 States  Judge Approves Anthropic’s $1.5 Billion AI Copyright Settlement With Authors

Judge Approves Anthropic’s $1.5 Billion AI Copyright Settlement With Authors  NIH Infectious Disease Leadership Shake-Up Raises Concerns Amid Ebola, Hantavirus Outbreaks

NIH Infectious Disease Leadership Shake-Up Raises Concerns Amid Ebola, Hantavirus Outbreaks  GSK Reportedly Nears $9 Billion Acquisition of Cancer Drug Developer Nuvalent

GSK Reportedly Nears $9 Billion Acquisition of Cancer Drug Developer Nuvalent

A court judgement handed down last Friday has delivered what years of promises from Australia’s life insurance industry have not – insurance that pays out on what it says it will.

I first raised the issue of outdated medical conditions within the insurance industry almost 15 years ago. Then in 2016, after stepping down as chief medical officer for CommInsure, then owned by the Commonwealth Bank, I spoke on Four Corners about the practice of using outdated definitions of conditions such as heart attacks to refuse payouts.

A random audit conducted of 40 heart attack claims found CommInsure had knocked back more than half by using a threshold for diagnosing substances in the blood that was by then out of date.

This then led to two parliamentary inquiries and an investigation by the Australian Securities and Investments Commission that found that while selling policies with outdated medical definitions was not against the law, it was “out of step with community expectations”.

ASIC belatedly got tough

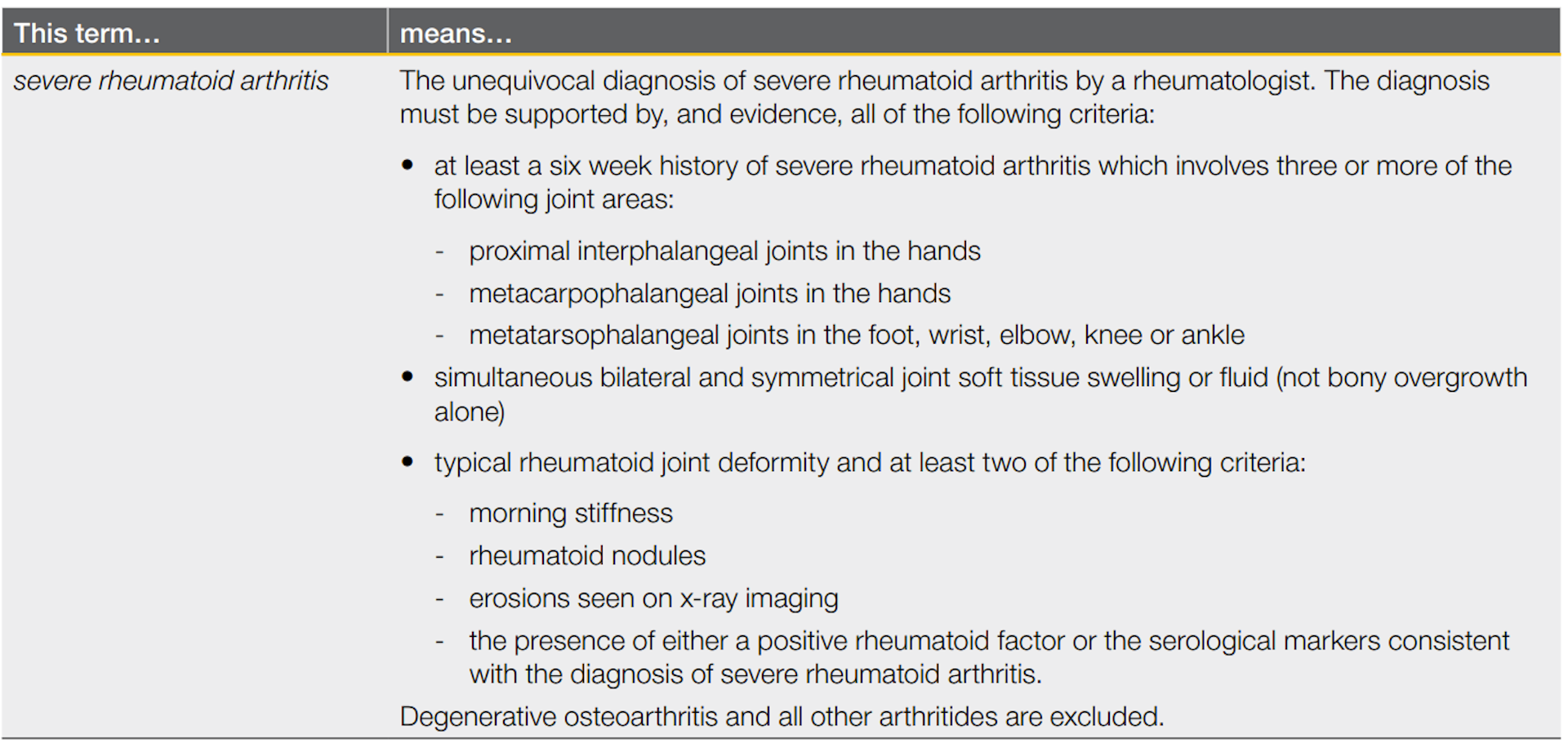

The banking royal commission was critical of ASIC’s performance in this area, and in 2021 ASIC commenced action against the insurer MLC for denying payouts to customers because it had failed to promptly update its definition for the insurance benefit of severe rheumatoid arthritis.

On May 18, Justice Moshinsky of the Federal Court found that MLC’s failure to promptly update the medical definition for severe rheumatoid arthritis had contravened the Corporations Act 2001.

The section of the Corporations Act in which the breach occurred has been in place for a long time, suggesting failure to update medical definitions would have been illegal for a long time.

Tight definitions quickly date

There are generally four types of life insurance in Australia. The most common is death (or more euphemistically, “life”) insurance, which pays a benefit when a policyholder dies. The others are

-

total and permanent disability insurance, which pays a sum of money when a person becomes disabled

-

income protection, which pays a monthly benefit when someone is sick

-

and trauma or critical illness insurance, which pays out a lump sum when a policyholder experiences a defined medical event.

For death insurance (“life” insurance) the definition is usually uncontentious, as it is for income protection insurance, which kicks in after a period of waiting if a treating doctor diagnosed a condition that prevents work in an occupation covered by the insurance policy.

Fine print can turn policies into junk.

More contentious are the definitions for total and permanent disability insurance and trauma insurance.

The problem with tightly and strictly-worded definitions is they can get out of date very quickly, whereas the policies they are written into can stay in place for decades. Unless updated, they can turn the policies into near-useless; so-called “junk insurance”.

The MLC policies that ASIC took action against required the claimant to develop a level of deformity now uncommonly seen, given available treatments – even for clinically severe cases. In essence what the court has found was that the holders of those policies were holding something close to junk.

Loopholes in the industry’s code

The Code of Practice for life insurers is only voluntary, and is administered by the Financial Services Council.

Insurers who subscribe to it now do have to review medical definitions at least every three years, but only for new policies that are currently on sale – not for existing policies held by existing customers.

The new code due to come into effect in July 2023 continues to leave out existing customers, but adds a commitment that seems to offer new customers more.

It says where a policy

has a medical definition which specifies an obsolete method of diagnosis or treatment that is no longer used in mainstream medical practice in Australia, we will assess your claim, including whether it meets the required degree of severity defined in your policy, using a current method of diagnosis or treatment approved for use in Australia

But for sufferers of severe rheumatoid arthritis the offer is near meaningless.

Whereas rheumatoid arthritis can be diagnosed by various clinical criteria, including blood tests, such diagnostic criteria does not equate to the level of severity.

The outdated definition of “severe” used in insurance policies commonly requires a number of things in addition to a diagnosis.

The extra requirements include (and all of them are needed) joint deformity, and bilateral and symmetrical joint soft tissue swelling or fluid.

These extra requirements are in addition to what is required for diagnosis, meaning that code, which refers to methods of “diagnosis or treatment” doesn’t cover them.

They are also obsolete, but the wording of the code only requires the updating of obsolete methods of diagnosis or treatment - not obsolete methods for determining severity.

Thankfully, claimants are now able to rely on more than the code. Friday’s judgement established that outdated medical definitions are a breach of the law regardless of the code, and have been for a long time.

{kind=link}