Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

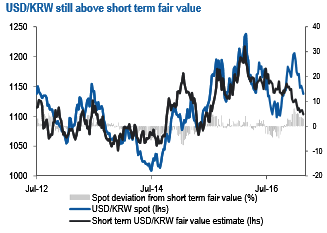

KRW still cheap relative to global reflation theme. At face value, we don’t believe all of the good news is priced in. The short term fair value model has taken another leg lower and now sits around the 1100 level (refer above chart).

For much of January/February, the fair value estimate was around 1110/1115 but renewed strength in local equities has pushed the fair value estimate lower (from a USDKRW perspective) over the past week.

Higher commodities since the start of the year have also been a factor, while yield spreads have broadly moved sideways over this period. We have seen spot USDKRW trend towards the fair estimate but there is still a reasonable wedge between the two series (albeit not as large as it was at the start of the year).

We still like to maintain longs in USDKRW 2m NDFs, so, initiate longs in USDKRW 2m NDF at 1156 with a target at 1245 (+5.3%) and a stop at 1133. The time horizon is 1-2 months and positive carry is approximately 2bp/month.

We retain our thesis that USD-EM has further upside in Q1. The KRW remains in the cross hairs of higher US yields, protectionism and geopolitics, a China growth slowdown and RMB depreciation.

Ongoing deterioration in rate differentials should keep the KRW trading on the back foot and negative forward points affords the opportunity to establish long dollar exposure with a positive (albeit small) carry profile.