U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different

Crude prices were mixed yesterday, as lower-than-expected inventories buoyed the U.S. crude grade while refinery maintenance in Europe weighed on oil prices in the region but tumbled sharply today, weighed by the U.S. dollar's recent rebound and as traders grew more cautious ahead of this week's U.S. supply data.

Currently, the total production growth in Canada/Alberta exceeds the takeaway capacity assuming the refineries are using upgraded bitumen and most of the non-upgraded bitumen is being exported. With Canada’s heavy oil production expected to rise further this year especially as Fort Hill coming online and expansion of CNRL’s Horizon 3 project adding to the heavy oil supply volumes in 2018, there is a sense of urgency to resolve the issue even if reluctance on both sides to compromise has so far lead to weaker spreads. The pipeline projects have either been delayed, canceled or not coming online soon enough. Shippers are relying on rail capacity and crude by rail has increased by 54% y/y in 2017.

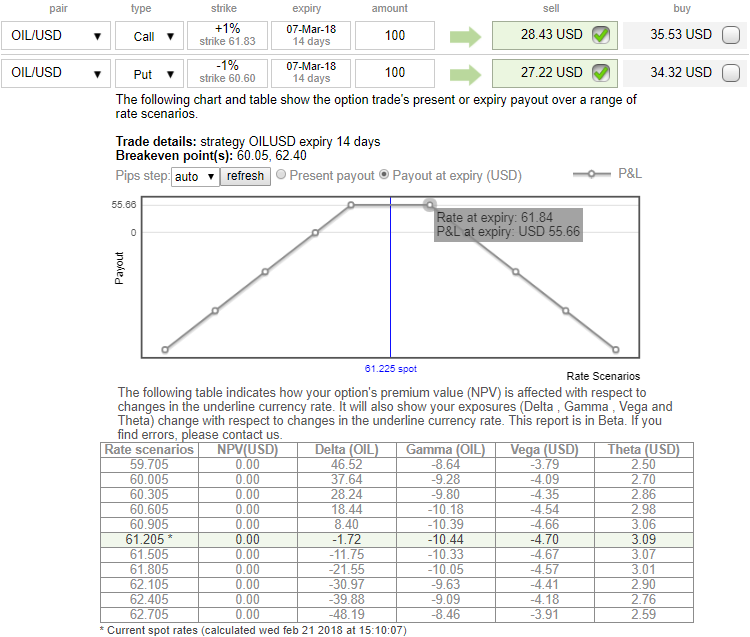

Contemplating above fundamental factors, we advocated below options strategies on both trading as well as hedging grounds.

Naked Strangle Shorting:

From last two months, WTI crude prices are stuck between $66.63 and $58.11 levels. Price momentum has been reduced from 3-4 days, and it is expected to remain same.

Hence, as shown in the diagram, short 2w OTM put (1% strike difference referring lower cap) and short OTM call simultaneously of the same expiry (1% strike referring upper cap) (we reiterate, comparatively short term for maturity is desired).

Overview: Slightly bearish in short-term but sideways in the medium term.

Timeframe: 2 weeks

When you write an option, the seller wants IV to remain lower level or to shrink so the premium also fades away which is what has been happening in this pair.

Hence, writing such calls seems smart choice in tepid IVs on speculative or trading grounds.

Considering above OTC market reasoning, amid prevailing uptrend we think downside risks can also not to be disregarded in the short term, as result we reckon deploying shorts in such exorbitant call options.

Call spreads:

Long in WTI, $68-75 call spread of December 2018 tenor is advocated as the increased financial market volatility is pressuring oil prices.

Given the still constructive view on oil prices in the coming months, we remain happy to stay long via a call spread. This is a cautious way to gain upside exposure to higher oil prices with limited downside.

Stay long a December 2018 WTI $68-75/bbl call spread (net premium: $1.40/bbl). Marked to market at $0.84/bbl, for an unrealized loss of 56¢/bbl, or -0.9% of the underlying.

FxWirePro launches Absolute Return Managed Program. For more details, visit: