Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

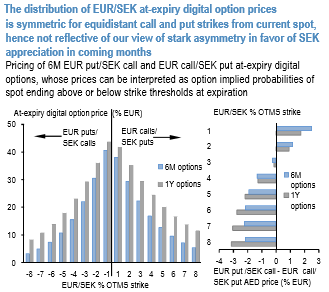

The FX option prices are not priced in the unambiguously positive asymmetry of Swedish Krona spot outcomes. Prices of at-expiry digital (AED) options would be construed as probabilities of spot ending at or beyond strike thresholds at maturity, and are useful for studying the option-implied likelihood of spot outcomes.

One side-effect of the correction in EURUSD has been that PLN and SEK, both of which we like, have fallen further against the dollar than the euro has. That’s not a new pattern and points to heavy positioning, as many people bought ‘euro-alternatives’ rather than the real thing, earlier this year.

The starkly positive asymmetry of SEK spot outcomes is not reflected in option prices. Prices of at-expiry digital (AED) options can be interpreted as probabilities of spot ending at or beyond strike thresholds at maturity, and are useful for studying the option-implied likelihood of spot outcomes.

SEK has long been tilted in favor of significant krona appreciation, albeit with uncertainty around timing given Riksbank's intransigence in adjusting ultra-loose monetary policy even in the face booming economic growth.

The above chart plots the implied distribution of EURSEK over 6-month and 1-year forward windows using EURSEK AED option prices for strikes of varying moneyness.

More than absolute probabilities of up or down moves that can be difficult to assess on a standalone basis, the standout feature of the plot is the lack of any discernible skewness in bullish and bearish outcomes; if anything, the RHS panel shows that strikes beyond ±2% from current market price EUR calls/SEK puts more expensively (i.e. more likely) than comparable % OTMS EUR puts/SEK calls, which militates against the balance of FX risks laid out above and is a textbook instance of disconnect between option market pricing and macro assessment of the spot distribution.

We favor buying zero-cost combinations of long EUR put/SEK call vs. short EUR call/SEK put digitals to position for an eventual normalization of Riksbank policy; for instance, off spot ref. 9.5275, 6M 9.20 EUR put/SEK call vs. 9.80 EUR call/SEK put at-expiry digital risk-reversal has a net premium credit of 2.7% EUR (-5.2 /2.7 two-way indicative. assuming equal EUR notionals/leg). The short strike is above the YTD high, hence reasonable cushion against a backup in spot. Courtesy: JPM