Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

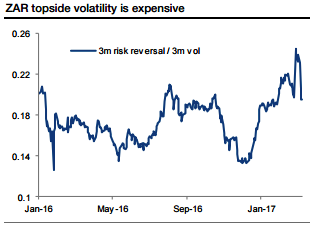

The implied volatility of the South African rand is the highest among EMFX space, though not unjustifiably expensive versus realized volatility, which makes any vanilla USDZAR put option expensive.

Skew is also elevated, with 3m 25d risk reversals being the highest across EM and in the upper half of the five-year historical range. The skew-to-ATM implied volatility ratio is at the top of the recent range, affording an opportunity to sell topside skew in a bullish ZAR structure.

Option mechanism:

Buy 3m USDZAR put strike 13.00 knock-out (KO) 14.20, indicative offer: 1.45% (vs 2.13% for the vanilla, spot ref: 13.0750).

The knock-out provides a 32% discount to the vanilla put option and also substitutes for a stop loss on outright short USDZAR exposure.

Risks profiling:

4% spike in next three months Investors buying a knock-out put cannot lose more than the premium paid.

However, the option will be worthless if USDZAR hits the 14.30 level at any time before the 3m expiry.

A strong payroll report could temporarily hurt the ZAR, and while a Fitch downgrade is partially priced in, it could cause another bout of temporary weakness.