Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

The strong Japanese IP report and business survey suggest solid momentum carried over into this year.

But, consumption appears to have been weak at the end of 2016, while the labor market looks favorable.

BoJ stayed on hold as widely expected; autopilot likely will continue at least until H2 of this year.

Abe would visit Trump next Friday, likely will try to persuade him that Japan is not a currency manipulator.

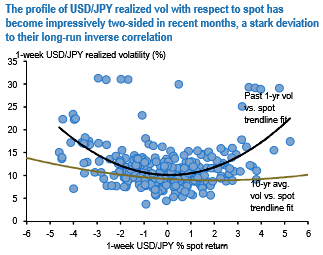

Aside from currencies buffeted by idiosyncratic factors (TRY, MXN, GBP), yen is the only other USD-major where owning vega has been profitable YTD. This owes primarily to USDJPY’s pronounced sensitivity to high frequency shifts in the US policy narrative since the November elections, both on the upside during phases of optimism around a muscular fiscal package and the attendant rise in Treasury yields, as well as on the downside when anxiety mounted around the Trump administration’s trade, tax and FX policy.

The latter does not surprise as yen appreciation and higher volatility during risk aversion is almost an axiom in currency markets; it is on the weaker yen side of the spot distribution that a new, higher volatility dynamic has emerged as US bond markets tantalizingly flirt with the prospect of breaking out of the post-GFC rate repression shackles.

There is also a flow angle to the story, in that perceptible leveraged macro-interest to position for USDJPY upside via options as a positive carry alternative to selling Treasuries has tended to generate a demand/ supply imbalance in the option market, which risks worsening if/when spot rallies towards 120 and prompts dealer demand for vega hedges against extant Japanese importer structures (e.g. knock-out forwards with barriers in the 125-130 zone).

The net result is a two-sided USDJPY realized volatility profile (refer above chart) that has proven relatively impervious to the direction of spot moves in recent months –unlike for most risk-sensitive currency pairs where spot vol correlation is well entrenched and has a distinct bias in favor of dollar strength – and is likely to persist as policy uncertainty in the US shows few signs of abating any time soon.