RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision

Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

On the eve of Bank of England’s monetary policy today, let’s begin by recalling as to how the UK central bank confused the markets in previous MPS. There was the widespread surprise when the MPC chose to leave rates unchanged in the last monetary policy meeting.

For now, there is no reason in pretending otherwise: the Brexit vote would be a hard blow for the UK economy in the months to come. Although the economy developed in Q2, the collapse in Q3 and forward guidance has been very painful.

The PMI in the UK has provided a first taster. Manufacturing sector eased significantly from 55.5 points in the previous month to the current 54.3 points; the final estimate now resulted in a real collapse (consensus 54.6). The PMI for the construction sector managed to produce upbeat flashes at 52.6 versus consensus at 51.9 and previous prints at 52.3, where service PMIs would be announced today but had collapsed from 52.9 to 52.6 in October and points in the same direction.

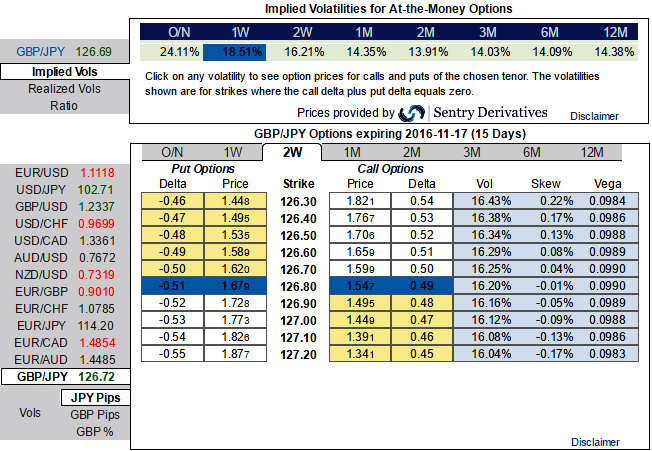

Please be noted that GBPJPY skew is not ready to smoothen too much ahead of central banks inflation report and monetary policy, the GBP volatility in 1-3m tenors normalized considerably.

The liquidity recovered and the extreme positioning was ultimately absorbed. The price action is not taking the direction of an imminent new trend. As a result, the option market aggressively unwound smile positions.

In our recent hedging portfolios we had advocated ITM put shorts when underlying FX price was at 127.35 levels, now you could probably guess that from the spot FX of GBPJPY, the yields from these shorts are certain by now.

Negatively skewed GBPJPY 1w IVs for now signify the interests of ATM put holders and their competitive edge in PRBS as an optimal hedge, consequently, we uphold -0.49 delta ATM puts.

Please be noted that the 1m GBPJPY IV skews are more biased towards OTM put strikes.

From the IV nutshell, one can understand that the negatively skewed IVs in 1m contracts would imply that the underlying spot FX is less likely to remain in ITM territory or in other words spot FX would shift towards OTM strikes.

There was also a valuation issue at play, in that yen, vols had lagged the sharp collapse in VXY prior to BoJ –held up in all likelihood by the outside chance of a policy regime shift in Japan –and were ripe for a sell-off if the meeting proved uneventful.