Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

Prices of the yellow metal are up nearly 15% so far this year as investors seek safe havens in the face of mounting instability in other financial markets

Technically, as we were discussing in our recent write up on this commodity, although the intraday bears are active it is advisable to carry short trades for deliveries as the intermediate trend seems uptrend and it looks like making a reversal of major downtrend.

It is evident that the bulls have managed to clear the major hurdle at 1225, 1294.50, and now at 1341.26 levels (i.e. 38.2% Fibonacci retracements from the bottoms of 1046.23 levels (see monthly graph).

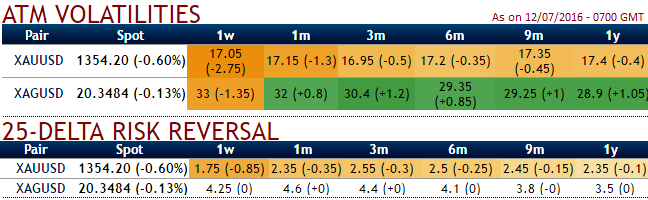

OTC Outlook:

ATM IVs of gold contracts across all tenors have reduced remarkably, it is considered as the good news for option writers.

While delta risk reversals are also flashing up with negative changes in bullish hedging arrangement especially the highest negative tickers during 1W expiries, we hope you may probably correlate this with the above-mentioned intraday downswings. With this OTC indication what we could empathize is that bulls have halted momentarily but intermediate uptrend still seems intact. As a result, we like to deploy below option strategy to deal with the baffling swings in spot gold prices.

Option strategy for Gold's puzzling:

The Execution: Contemplating both fundamental and technical reasoning in mind, it is advisable to go long in 2M (1%) OTM 0.36 delta call while writing 2W (1%) ITM call with positive theta and delta closer to zero (both sides use European style options), this credit call spread option trading strategy is recommended when the gold spot price is anticipated to drop moderately in the near term and spikes up in long term.

Trade expects that the underlying gold spot price would drop to ITM strikes on expiration and thereafter bounce back again.

Thereby, you are speculating the gold's struggle in the short run by shorting, and hedge any dramatic upside risks in the long term via longs in OTM strikes which is why we've used diagonal expiries.

Margin: Yes for ITM shorts.

Return: The return is limited by ITM shorts. No matter how far the market moves below that point, the profit would be the maximum to the extent of initial premiums received.

BEP: The break-even point lies between ITM and OTM strikes.

Risk: If the underlying spot gold price rises above the strike price of the higher strike call at the expiration date, then this bear call spread strategy likely to suffer a maximum loss equals to the difference in strike price between the two options minus the original credit taken in when entering the position.