Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

Collect theta on AUDUSD and USDCAD vol ratio spreads traded via Gamma timing filter:

Risk premium harvesting via traditional straddle selling can be a challenging proposition when spot gyrations pose risk in front-end tenors and inverted curves challenge executing it in the back tenors. A close but a safer alternative is 1*N ratio call or put spreads (delta-hedged) on the rich side of the skew as a class of structures that can monetize risk premia in vol smiles. Placing the short notional overweight on the “risk-off” side, these structures sell risk-reversals resulting in quick collection of premium but are exposed to left tail and thus suitable only when there is no imminent risk from sell-offs.

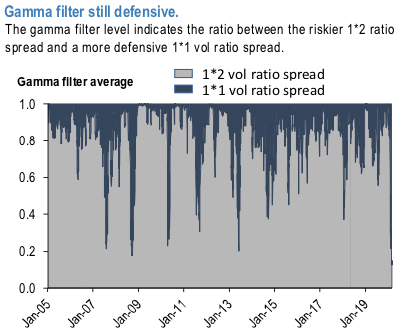

To solve the left tail issue we follow on the heels of our prior work on gamma trading filter (Total-return version of tactical filter allowing long Gamma trades) and utilize the filter in vol ratio spreads trading. The model relies on a set of common global indicators and along it currency specific variables that assess level of risk-aversion in the broad markets. We use the gamma timing filter to determine the notionals split between 1*2 vega ratio spreads and M/N (market neutral) ratio spread. The G10 average filter signal as given in the 1st chart is always within (0,1) range. The value of e.g. 0.75 means that 75% of the notional goes toward 1*2 and 25% into M/N risk ratio structure.

The historical average has been around 87-88% across currencies. The switching methodology is admittedly crude and could be optimized for different splitting formula, introduce thresholds, and/or optimize choice of structures. The long-term backtest in 2nd chart shows a clear benefit from utilizing the filtering methodology, with the volatility of returns materially improved as the max drawdown is cut by almost 50%.

One intuitive way for screening for the currencies with the most favorable backdrop for 1*2 vol spreads is to look at the following: a) medium-term performance, e.g. 3-year Sharpe, and b) current pricing of the 1*2 structures expressed as 1-y zscore of skew / ATM vol ratio.

Among the USD pairs at the current markets, the high beta G10 AUD, NZD and CAD screen the most attractively (the upper right quadrant in 3rd chart) thanks to the elevated skew vols, but the gamma filtering strongly suggests to express the structures via 1*1 vol ratio spreads rather than the more aggressive 1*2s. Courtesy: JPM