Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

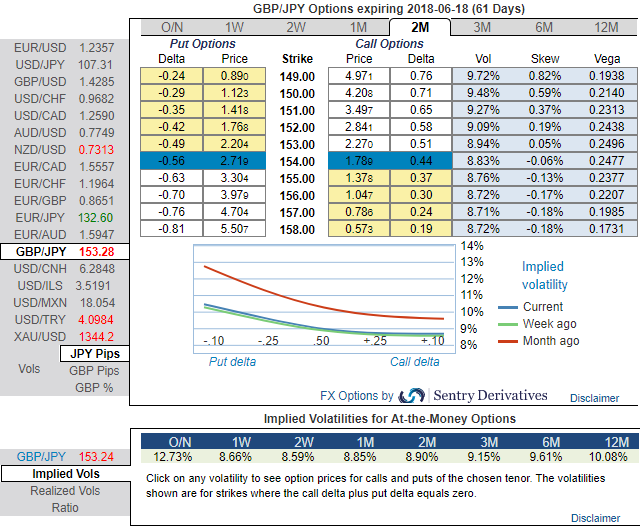

GBP’s performance in January was stronger than we had expected on a combination of less immediate tail risk from Brexit(following outline political agreement in December over a stand-still transition once the UK leaves the EU next March until end-2020) and a more supportive central scenario for the economy and monetary policy. Of the two, a reduction in the Brexit risk premium appears to have been the more significant.

Nevertheless, the modest acceleration in UK growth to around 2% doubtless contributed to the reversal of speculative positioning in GBP from heavily short to heavily long (more so CTAs than macro investors we believe) as it led to a firming up of UK rate expectations (one and a halfhikes are now priced for the end of 2018, three and a half by end-2020) and the promotion of GBP to the vanguard of currencies where central banks are in the early stages of policy normalisation.

GBPJPY has been spiking more than 38.2% Fibonacci retracements in the consolidation phase in the major declining trend. However, one month has been enough to wipe-off previous 5-months’ rallies (refer monthly plotting for February’s price slumps). This shows the intensity of the major declining trend.

To substantiate this bearish stance, let’s glance at the positively skewed IVs of GBPJPY of 2m tenors still signify the hedgers’ interests in OTM put strikes (upto 149 levels) and isn’t this a luring factor for a shrewd bear. While 2w/2m IVs of ATM contracts are trending above 8.59% and 8.90% respectively that are the suitable combinations for diagonal ratio spreads structures.

Because the higher IVs with well-adjusted positive skewness signify the hedgers’ interest for both OTM call/put strikes. In usual circumstances, long option position needs higher IVs for significant change in vega. Hence, we capitalize on buzzing IVs in 2m tenor for long leg and improve odds on options below strategy.

The aggressive volatility investors want to capture GBP should consider buying ATM put instruments and/or being long of the smile convexity, against ATM volatility. Thus, ATM strikes are perceived to be more conducive than the OTMs.

Further GBPJPY upswings and/or weakness suggest building directional strategies as given below and volatility patterns at the same time.

1) In order to mitigate the mounting downside risks and keep them on the check, we advocate adding longs in 2 lots of (1%) OTM -0.49 delta puts of 2m tenor while writing 1 lot of 1% ITM put of 2m tenor. Payoff structure of this strategy has been exponential as the underlying spot FX keeps dipping (refer above payoff table).

Contemplating IV skewness and ongoing technical trend, we foresee the value of ATM options would likely rise significantly as the IVs seem to be favoring long legs of ATM strikes.

2) Dubious and risks averse traders, we advocate buying GBPJPY – USDJPY 1Y ATM straddle spread with equal JPY vega.

3) Alternatively, on hedging grounds, we advocate shorting futures contracts of near-month tenors as the underlying spot FX likely to target southwards 145 levels in the near run and 146 levels in the medium run.

Writers in a futures contract are expected to maintain margins in order to open and maintain a short futures position.

FxWirePro launches Absolute Return Managed Program. For more details, visit: