China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

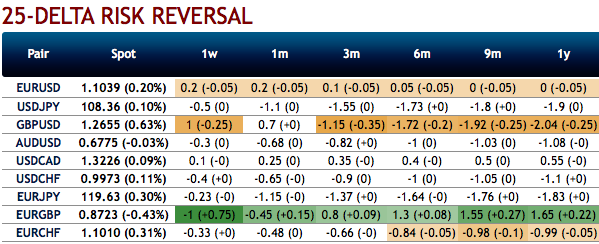

The primary motivation for these trades was poor European growth momentum as also reflected in the weak flash PMIs, which was expected to weigh on cyclical economies with strong links to regional growth. Thus, EURGBP shorts have been recommended in part due to carry and in part due to global growth apprehensions and the recent Brexit developments that have kept us bullish.

Soft regional growth continues to be a dominant concern for the Euro bloc. Following the abysmal Euro area flash PMIs to substantiate, while the activity data has continued to disappoint and the economic activity surprise indices are negative in the Euro area. The economists’ growth forecast revisions have been negative as well over the past quarter (for the Euro area and Scandis).

Amid the prospects of an interim US-China trade deal as well as increasing possibility a Brexit deal in the run-up to the October 31st deadline, we see EURGBP’s interim price dips are momentary and it is wise to capitalize on them to deploy longs in the long-run.

Let’s now quickly glance through OTC outlook before looking at the options strategies. Fresh positive numbers are added to bullish risk reversals of EURGBP. This is an indication of the broader hedging sentiment for the bullish risk outlook in the FX OTC markets, this is interpreted as the hedgers are keen on bullish risks but with the mild downside risk sentiment in the near-term (refer to negative risk reversals in 1m).

While the passively skewed IVs of 3m tenors are stretched are indicating upside risks, more bids are observed for OTM call strikes up to 0.92 level.

While EURGBP risk reversals of the existing bullish setup remain intact with mild bearish shift, you see minor negative risk reversal numbers, but it should not be perceived as the bearish scenario changer. Instead, below options strategy could be deployed amid the expected turbulent condition.

According to the OTC FX surface, 3-way options straddle versus ITM calls are advocated seem to be the most suitable strategy for EURGBP contemplating some OTC sentiments and geopolitical aspects.

Options Strategy: The strategy comprises of at the money +0.51 delta call and at the money -0.49 delta put options of 2m tenors, simultaneously, short (1%) ITM calls of 1w tenors. The strategy could be executed at net debit but with a reduced trading cost.

Hence, on hedging as well as trading grounds, initiate above positions with a view of arresting potential FX risks on either side but slightly favoring short-term bearish risks.

Alternatively, on hedging grounds we advocated initiating directional hedges that comprised of shorts in EURGBP futures contracts of September’19 delivery and simultaneously, longs in futures of December’19 delivery for the major uptrend, we wish to maintain these positions.

We wish to maintain the same strategy by rolling over short-leg of October delivery, while the long-leg remains intact. Courtesy: Sentrix, JPM & Saxobank