European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic

Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  China Extends Gold Buying Streak as Reserves Surge Despite Volatile Prices

China Extends Gold Buying Streak as Reserves Surge Despite Volatile Prices  Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness

Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness  Bank of England Expected to Hold Interest Rates at 3.75% as Inflation Remains Elevated

Bank of England Expected to Hold Interest Rates at 3.75% as Inflation Remains Elevated  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

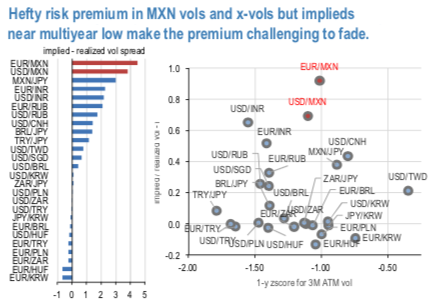

MXN realized vol is at historically low levels, resulting in eye catching MXN and x-MXN implied – realized vol spreads within the EM space (4.5vol and 3.8vol for EURMXN and USDMXN, respectively). Despite the hefty risk premium (refer 1st chart), with the implieds at multiyear low we prefer cautious constructs that monetizes vol smiles premium instead of outright vol shorts. 2m realized spot- vol correlation plunged as August rolled off from the 2m trailing window while 25 delta OTM MXN puts / ATM remain 1-sigma extended (1-year z-score basis).

Further expected policy easing by Mexico’s central bank and limited regional data will probably have the overall region more influenced by spillover effects from global developments over the coming week.

Banxico is expected to cut its overnight rate by another 25bps on Thursday.

It is analysed that earning theta without taking left tail risk via high beta ratio call spreads. Such structures are covered to a fair extent against spikes of high beta volatility given the long risk-reversal sensitivity embedded in the structure. Considering the current MXN skew setup and the receding risks for MXN spot we are open to taking the gamma risk in order to more efficiently reap the extra OTM vs ATM premium on MXN put side. 1*1.5 MXN ratio put vol spreads have shown strong and almost equivalent systematic returns for USDMXN and EURMXN over last few years (refer 2nd chart).

Consider: 3M EURMXN ATM/25D 1*1.5 vol ratio call spread @9.45ch vs 10.5/10.75 indicative.

3M USDMXN ATM/25D 1*1.5 vol ratio call spread @9.4ch vs 10.45/10.65 indicative. Courtesy: JPM