BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

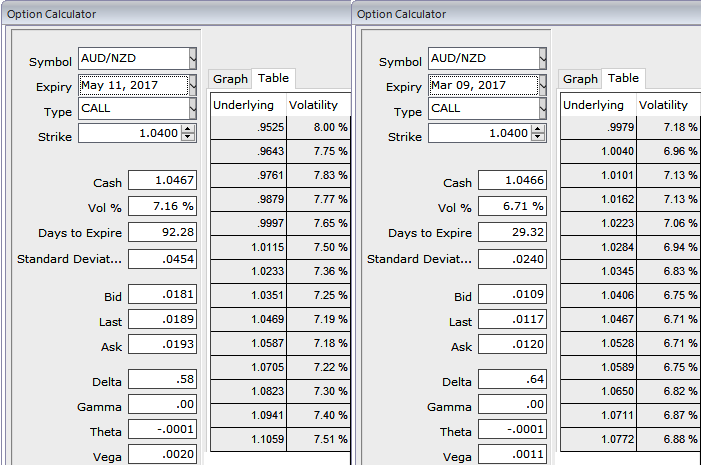

AUDNZD downward momentum persists despite recent bull swings, amid abrupt rallies the next major target 1.0326 (recent lows) and 1.0238 can also not be disregarded.

The pair in medium term perspectives: Higher to the 1.0650-1.0770 area, mainly for valuation reasons. The cross remains well below fair value estimates implied by interest rates, commodity prices, and risk sentiment.

Please be noted that the implied volatility of at the money contracts of this APAC pair has been trading at a tad below 6.7% and 7.16% for 1m month 3m tenors respectively, while vega instruments of 3m tenor are signifying the hedgers’ interests in downside risks.

So, the speculators and hedgers for bearish risks are advised to optimally utilize the upswings in short run as the lower implied vols are conducive for option writers, accordingly, we had advised ITM shorts in put ratio back spreads and as the underlying spot FX has risen a bit, the writers could have pocketed the premiums that they have received from these shorts.

AUDNZD's lower IVs with theta’s interest on ITM put strikes could be interpreted as the option writer’s opportunity in short run.

The two main risks to our bearish AUD view are that (1) the currency is dragged higher in a more sustained re-rating of the global growth outlook and that (2) better global news and some signs of housing resilience see the RBA play for time. RBA has maintained status quo in last monetary policy to maintain the cash rates at 1.5% but we remain of the view that the RBA will ease a further 50bp going forward.

On the flip side, RBNZ should cause few ruffles in the market, with the policy stance (on-hold with a neutral bias) likely to be retained. That is because the positive impulse from dairy prices is roughly offset by the higher NZD TWI and higher funding costs. The RBNZ’s OCR projection should remain unchanged at 1.7%. But New Zealand remains highly exposed to a slowdown in Chinese demand, and the RBNZ won’t stay neutral in front of revived currency strength.

Weighing up all above aspects, we eye on loading up with fresh longs for long-term hedging, more number of longs comprising of ATM instruments and ITM shorts in short term would optimize the strategy.

So, the execution of hedging positions goes this way:

Go long in 2 lots of long in 3m ATM +0.49 delta put options, simultaneously, stay short 1m (0.25%) ITM put option, the position may gain if the underlying spot abruptly shows any mild gains. The strategy should be constructed at net debit with net delta at around -0.45.