Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks

RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

The Swiss National Bank (SNB) abandoned its minimum exchange rate in January 2015 stating that it did not want to accept the further massive increase of its balance sheet total. Even though it has managed to stabilize EURCHF on the FX market with the help of cautious interventions risk events such as the Brexit referendum or the US Presidential elections illustrate clearly that from time to time the SNB still has to intervene quite heavily against the franc.

As a result, the SNB’s sight deposits and FX reserves have risen notably again. That means its balance sheet has continued to expand and its strategy has failed.

On the other hand, the SNB has reached the limits of its monetary policy scope as it has lowered interest rates into negative territory, which stand at -0.75%. A further rate cut to weaken the franc would only fuel cash holding. The SNB would initially stick to its monetary policy so that EURCHF would trade in a range around 1.08.

On the other hand, it will have to decide at some stage whether to prevent franc appreciation so as to maintain its inflation target or whether to consider the rise in FX reserves to constitute the bigger risk, which means stopping its interventions.

We think the inflation target will again draw the short straw which means that EURCHF would collapse at some stage. The timing, on the other hand, is difficult to predict.

OTC updates and option strategy:

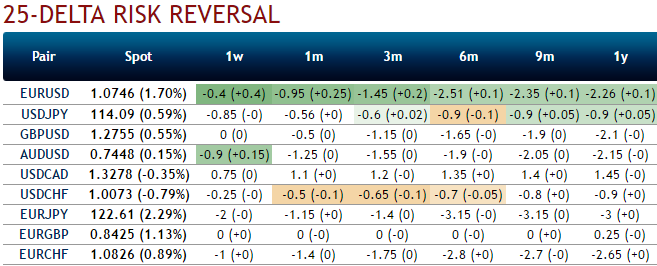

If you glance through the IV nutshell, the implied volatilities of EURCHF ATM contracts across all expiries (especially 3m-6m) have been the least among G10 currency segment.

While the 25-delta risk of reversal of EURCHF has been indicating hedging sentiments for the downside risks, as a result it indicates puts have been relatively costlier.

Option-trade recommendations:

EURCHF’s range bound pattern is still persisting (Ranging between upper strikes 1.1110and lower strikes at around 1.0725 levels.

We could still foresee range bounded trend to persist in near future with upside potential in short term but the trend likely to remain very much within above stated range.

As a result, we recommend below option strategies using right options, thereby, one can benefit from certain returns as long as the underlying remains between the strikes chosen in the strategy on expiration.

Naked Strangle Shorting: Short 1m OTM put (1.5% strike difference referring lower cap) and short OTM call simultaneously of the same expiry (1.5% strike referring upper cap) (we preferably choose short-term maturity).