2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

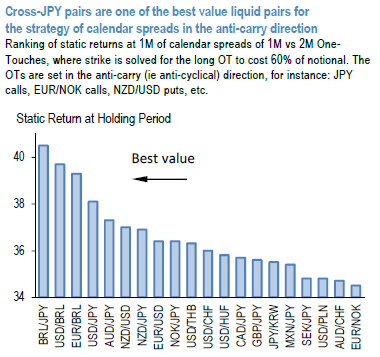

Amid the marginally more cautious backdrop below we review some limited downside and RV opportunities. We advocate monetizing the current AUDJPY curve set-up via short 1M vs long 2M one-touch calendar spreads, capped loss vol selling constructs that offer better gearing than outright one-touch shorts.

While August liquidity has potential for staging a surprise or two the flat or even modestly inverted vol curves offer an opportunity for scooping the recent build up in risk premia as softening realized vols drag short-dated implied vols lower or simply financing longer term view by selling the premium rich front expiries i.e. as an efficient way of owning tail-risk. While clearly subject to path dependence in spot, one-touch (OT) calendars are levered vehicles for milking theta via the front-end option short, for a small upfront premium commitment that also constitutes the maximum capital at risk when set up with identical strikes and notionals on both legs (such that one cancels the other in the event of barrier knockout, resulting in a net zero liability).

The 1st exhibit ranks -1M/+2M one-touch calendars based on their static return at 1m holding (i.e. at expiry of short leg). Cross-JPY pairs screen as one of the best value liquid pairs. We advocate monetizing the AUDJPY curve set-up via short 1M vs. long 2M one-touch spreads, capped loss vol selling constructs offering better gearing than outright one-touch shorts.

For instance, a 1M 73.90 strike no-touch (or selling a 1M 73.90 strike one-touch) delivers a maximum gearing of 1.6X (100% max payout / upfront cost of 60%). In comparison, a short 1M 73.90 vs. long 2M 73.90 one-touch calendar spread costs around 11%, and delivers a static leverage of 3-4X (refer 2nd chart). The robust 3Y historical performance of -1M/+2M at 1-mo holding is supportive (refer 3rd chart). Moreover, the backtest shows only marginal underperformance of the structures with notionals set in such way that the premium is returned if both OTs trigger. This rebate version of the OT spread increases the cost of the structure, thus lowering returns on premium.

Consider:- Short 1M AUDJPY 73.90 (40% TV) one-touch put vs long 2M AUD/JPY 73.90 one touch put @10/13%, spot ref 75.85 Or in form asymmetrically weighted calendar so that in case of the barrier getting knocked-in the holder gets paid the premium back: - Short 1M AUDJPY 73.90 (40% TV) one-touch put vs long 2M AUDJPY 73.90 one touch put in 0.8:1 notionals @18/21%, spot ref 75.85 levels. Courtesy: JPM