AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110

AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: AUD/USD drifts lower, uninspired by jobs beat

FxWirePro: AUD/USD drifts lower, uninspired by jobs beat  FxWirePro: NZD/USD extends losing run, eyes 0.5600 level

FxWirePro: NZD/USD extends losing run, eyes 0.5600 level  FxWirePro: USD/CAD uptrend loses steam, remains on bullish path

FxWirePro: USD/CAD uptrend loses steam, remains on bullish path  FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet

FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: USD/ZAR remains buoyant, looks to extend gains

FxWirePro: USD/ZAR remains buoyant, looks to extend gains  BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts

BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts  FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path

FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path  FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop

FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop  FxWirePro: GBP/NZD gaining momentum for a move towards 2.3100 level

FxWirePro: GBP/NZD gaining momentum for a move towards 2.3100 level  FxWirePro:NZD/USD rout continues without relief

FxWirePro:NZD/USD rout continues without relief  FxWirePro: USD/JPY dips as Japanese Yen consolidates near 40-year low

FxWirePro: USD/JPY dips as Japanese Yen consolidates near 40-year low  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro: GBP/AUD sustains gains as uptrend remains strong

FxWirePro: GBP/AUD sustains gains as uptrend remains strong

We could foresee that the recent sharp rally in the precious metal's price is a selling opportunity. The gold price seems to be discounting no further Fed rate hikes this year and very little tightening next year.

The precious metal has been bouncing consecutively especially with a sentiment of "safe haven" among all asset classes from last couple of weeks but as stated in our earlier apart from that we see no fundamental reasons to substantiate these price bounces.

China's imports of gold from Hong Kong slumped to the smallest since 2011 in January after surging to the highest level in more than two years in December, as global prices climbed the most in a year.

Net purchases by the world's largest consumer fell to 17.6 metric tons from 111.3 tons in December and 71.6 tons in the same month last year, according to data from the Hong Kong Census and Statistics Department compiled by Bloomberg.

The gold on the Comex division of the NYME for April delivery has stapled by $4.50, to trade at $1,239 a troy ounce by 10:00GMT. Prices of the yellow metal hit a one-year high of $1,263.90 just a few days ago.

Our economists expect the US economy to withstand the slowdown in emerging markets, and this should over time cause the market to price in a moderate pace of Fed tightening.

Also, the recent gold price rally looks unsustainable given the strength of the US dollar, keeping in mind their broad inverse relationship. Finally, the recent very pronounced downtrend in the BCOM index suggests that the gold price rally is unsustainable.

Although, the gold futures rose in European trade on Tuesday, with prices re-approaching the highest level in a year amid mounting expectations for further stimulus measures from central banks in Asia and Europe may carry huge uncertainty in its trading.

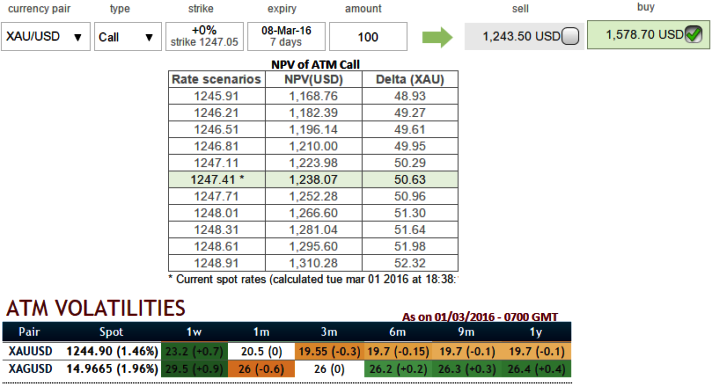

Hence, we recommend bullion traders to stay hedged using below commodity option strategy.

Hedging Framework:

3-Way Options straddle versus Call

Spread ratio: (Long 1: Long 1: Short 1)

Rationale: ATM premiums are trading 27% more than NPV, while implied volatility of these ATM 1W contracts are at 23.2%, hence there exists a considerable disparity between premiums and vols that keeps us eye on shorting such expensive calls. As a result, we capitalize on such beneficial instruments and deploy in our strategy.

How to execute:

Go long in XAU/USD 3M At the money delta put, Go long 6M at the money delta call and simultaneously, Short 3M (1.5%) out of the money call with positive theta.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: No fundamental rationale for yellow metal to swing up - hedge via 3W straddle vs call on disparity between premiums and IVs

Tuesday, March 1, 2016 1:20 PM UTC

Editor's Picks

- Market Data

Most Popular