UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

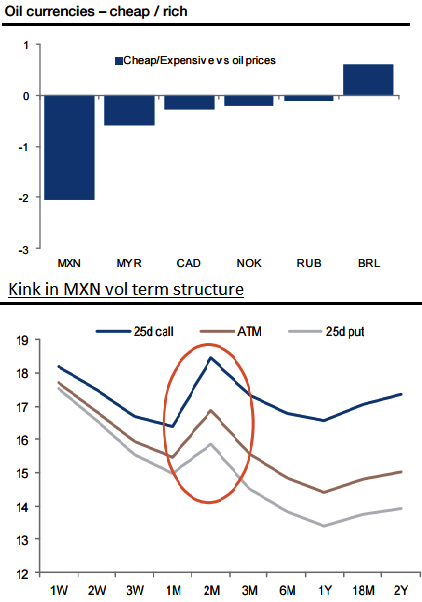

The MXN is around two standard deviations cheap versus oil prices as you can observe in the above chart (based on a weekly regression of FX and oil prices since 2014), while the rest of G10 and EM oil-driven currencies are within 0.5 standard deviations.

The risk premium in the MXN seems related to US politics, and specifically a non-negligible chance that Trump wins in November. Risk premium is not discernible in other currencies or asset classes.

Given the potential sensitivity of the MXN to a Trump victory, the term premium is most noticeable in USD calls. By comparison, the risk premium around the US election is non-existent in other EM currencies.

Selling MXN vol and buying vol in other EM currencies that might come under pressure (KRW, TWD, and TRY) might be worthwhile to consider.

In US election: impact on currency markets we analyse five transmission channels to build an EMFX Trump-vulnerability index.

There is a distinct kink in the MXN vol term structure between the 1m and 3m tenors that straddles the US election (November 8).

EM currencies fear Trump. The ZAR, MXN and MYR have been most sensitive to improvements in Donald Trump’s poll results.

Hence, short AUDMXN to fade US political risk premium and capture MXN being cheap vs. oil and AUD expensive vs. rate differentials (link).