With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

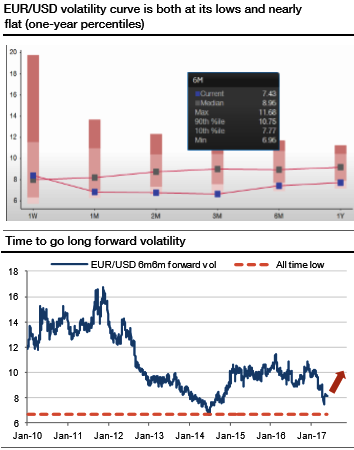

After the French presidential election, the EURUSD volatility curve aggressively sold off, reaching its lowest level since 2014. Since then, implied vols have bounced only very timidly and are still very close to their recent lows (refer above graph). Interestingly, the curve is usually quite steep when vol is globally low, and conversely, it tends to flatten or even invert when vol rises. The current configuration – a nearly flat curve combined with low volatility – looks like an anomaly, as the vega part should include a term premium when the front end is very low.

Curves are usually driven by the front end, and the risk priced there is then diffused towards the longer tenors. But even if short-term volatility remains subdued, we can contemplate the steepening being driven by the vega part of the curve in a context where the market is not shaken by near-term fears but starts discounting the medium-term outlook. EURUSD 6m volatility in six months offers a great opportunity, as it is trading only about one volatility point above its all-time low (refer above graph).

The uncertain and reflationary environment should involve a premium in vega vols, with the flat curve making forward volatility very attractive to buy. We recommend going long an EURUSD 6m6m forward volatility agreement at 7.8.