Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

No doubt from last two weeks, USDCNY has been spiking higher to the current levels of 6.5954 from the recent lows of 6.4345 levels.

However, it is foreseen that the strength of CNY can be traced to three factors:

The rebound in real GDP, higher commodity prices (which has aided the reflation theme and reduced pressure on the banking system) and higher interest rate differentials.

At the same time in recent months, our proxy of FX positioning data indicates that Chinese corporate USD selling interest has risen noticeably.

To the extent that this positioning adjustment is not yet complete suggests we could still further downside pressure in USDCNY in the near term.

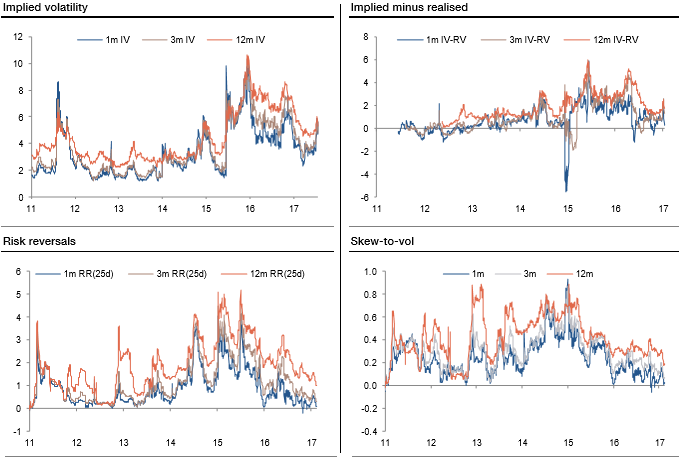

The implied volatility has bounced off the recent lows, the richness of implied versus realized vols has eroded; risk reversals and skew-to-vol are falling, term premiums have compressed while the vol smile has moved higher.

The base case scenario envisions CNH outperforming the forwards to year end.

However, a near term correction might ensue if EUR/EM FX falls or the Party Congress disappoints on the growth front. The PBoC has shown unease about USDCNH being much below 6.50. Topside exposure coupled with selling a downside strike (i.e. bullish seagulls) could be an appropriate structure.