Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings

Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

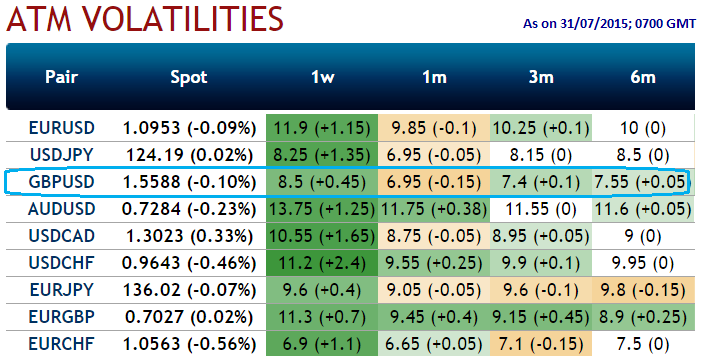

Since the GBPUSD's implied volatility is perceived to be comparatively minimal among the major currency basket (experienced at 8.5%) and expected to be lower over the period of time as shown in the nutshell, so contemplating this IV one can execute the calendar straddle as follows, It is quite simple as we go shorts on ATM calls and ATM puts using near month contracts while adding longs on far month ATM calls and ATM puts again from the rapid time decay of the near term options sold. It is likely to fetch certain returns to the extent of premiums received but offers limited risk to the options trader who thinks that the GBP/USD exchange price will experience very little volatility in the near term.

So streaks of questions arise how to monitor these multiple legs strategy, similar to all calendar spreads it is very essential to decide on which follow-up action to take when the near-term contracts expire. This is exclussively dependant on the revised outlook of the GBP/USD at that time ahead of Fed's rate policy. Should the options trader reckons that the underlying volatility will likely remain low, then another calendar straddle by writing another near term straddle is advisible.

If he thinks that the volatility is likely to increase significantly, he may wish to hold on to the long term straddle to profit from any large price movement that may occur. However, if the options trader is unsure of what to expect of the underlying, it may be best to take profit (or loss) and move on to evaluate other trading possibilities.