Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

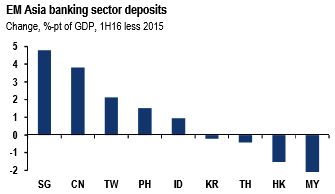

This week we examine local currency bank loan and deposit trends across the region. Similar to the deleveraging in external debt noted in last week’s focus, domestic loan growth has remained relatively weak, likely reflecting softer credit demand resulting from subdued economic growth and declining trade growth. Slower loan growth has kept loan-to-deposit (LDR) ratios broadly flat in the region ex. China and India.

In Asia, the declines in local currency deposits have stabilized somewhat as demand for FX deposits decreased and USD depreciation broadened in the first half of the year (see above diagram).

With the next Fed rate hike appearing imminent, USD has strengthened notably in recent weeks, which if sustained may limit local currency deposit growth and keep banking system liquidity tight in the region.

We advocate investors having neutral exposure to EM FX and refraining from large risk allocations heading into the US election. Our portfolio of trade recommendations should be well insulated in either scenario, focusing on a mixture of short and long USD trades and inter-EM relative value positive carry structures.

In Asia, we like short USDIDR and long USDTWD and relative value positive carry structures that include short MYRIDR, short SGDINR, and long INRKRW.

In China, we continue to recommend owning 1-year USDCNH seagull structures and shorting CNH against an abridged CFETS basket.

Apart from Asian pool, the favorite Trump hedge is to own a USDTRY 3.16 call with a KO at 3.41.