Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

As the US president, Trump escalates trade war in Q3, in the latest twitter tirades and his latest appearances in front of his supporters the US President has indicated something akin to a “strategy” behind his trade war policy. He is for example pleased about the weak Chinese stock market, as if that was a positive signal for the US economy. What is even worse: by giving tariff revenues a central role in fiscal policy the US President illustrates that his “tough approach” does not aim at enforcing a half-way amicable agreement. The trade war will remain in place regardless of how much the Chinese cave in. It is a means to a completely different end: of whipping in his followers. That makes the question of the consequences for USD exchange rates even more relevant.

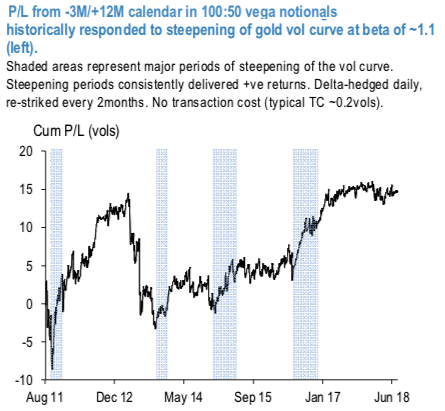

Amid this macro-level development, historical performance of XAUUSD vol calendars (the above chart) shows a consistently good track record during vol curve steepening episodes, with 1.1 beta of returns to vol pts of steepening. 12M-3M should widen by about 1.1vols in order to mean-revert to its 1Y average (from the currently 2 sigma too narrow gap); a rough assessment of the mean- reversion speed of the vol spread places its half-life at around 2.5 weeks which, being well below the maturity of the short leg of the spread, should give enough time for the term-structure dislocation to correct.

Moreover, at current market the structure is showing 2vols of vol carry from the short front-end straddle. Accounting for both P/L components (vol curve and implied-realized gap) in a multivariate historical regression we estimate >1.6vols of potential gain, while 1Y @10.7vols and at a historical low should limit the downside. With the latest positive turn in trade developments, one potential near term risk to the short front vol leg that still remains was the recent GDP print.

Still, given the tight risk-reversals, implying a spot/vol correlation near zero (at 7%), large moves in the spot should not overly impact the front-end of the curve and trigger a further tightening of the 1Y-1M spread.

To summarize, with the current gold surface dislocation mostly concerning the elevated front end vols and a sizeable implied-realized gap we overweight the short vol front leg:

Sell 3M @9.45 choice vs buy 1Y @10.3/10.65 indic XAUUSD straddles in 100:50 vega notionals, keep delta-hedged. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index is inching towards 93 levels (which is bullish), while articulating (at 14:38 GMT). For more details on the index, please refer below weblink: