European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025

Whatever be the driving forces, whether it is mounting geopolitical issues or global economic slowdown or anything else, the underlying price of any asset class is a function of demand/supply equation ultimately.

While we have already stated that the demand for bullion space appears to be down-casted in Asian regions on account of economic slowdown, natural calamities in countries like India and most importantly, rising prices have all hampered the consumer buying sentiments, even if attractive discount offers is luring buying interests on the eve of the major festival season in the region.

Bullion prices in India (Gold & Silver futures), the one of the largest bullion consumers after China, is trading at around Rs.38,464/10 grams at MCX (while articulating), easing -0.09% from previous close, while silver is trading at Rs.45,938 level for December 2019 delivery.

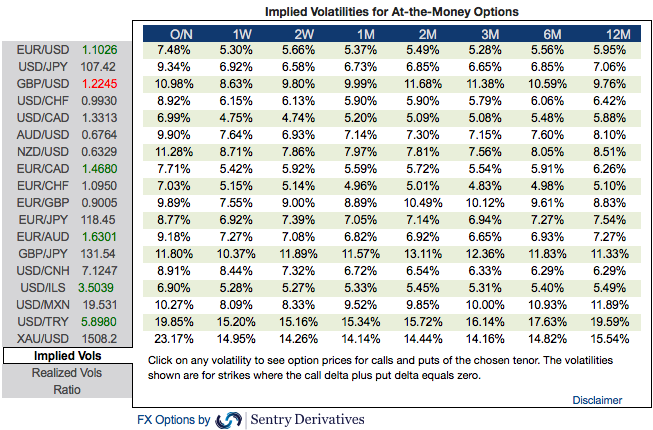

In our recent post, we raised a cause of concern for Gold’s (XAUUSD) rallies in the short run. Accordingly, the yellow metal prices seemed little edgy, the price dipped below $1,500 an ounce before it staged for the prospects of 6-1/2 years highs.

Gold 1M ATM vol rose slightly over the past week as the spot price also surged considerably back up above $1,500 levels. In a recent report, we used JPM’s regime-based model (Hidden Markov Model) to analyse the dynamics of GVZ, (i.e. the ‘Gold VIX’ Index).

This index is calculated using the same methodology as the VIX but uses the ETF GLD instead of the S&P 500.

Where we observe that when imposing a 3-regime model on the gold VIX, the 3-regimes (which we call low, medium, and high) that the model produces have means of 12, 17, and 27, respectively. Furthermore, the boundaries are 14, and 21 and the model spends roughly 28%, 44%, and 28% of the time in each of the regimes.

Currently the GVZ is at 15.26 and since we find that the GVZ level tends to get ‘stuck’ in its regimes, our model expects that it is more likely for GVZ to tend towards it current regime’s mean of 17 as opposed to falling below 14 into the lower regime. The previous analysis is one reason we prefer to go long on gold vol.

Most importantly, positively skewed 3m IVs of XAUUSD indicate upside risks, bids for OTM calls reveals that intensified buying momentum in the underlying spot prices. In addition, the positive risk reversal numbers also substantiate the same hedging sentiments.

Another reason is that the gold spot price projection which points towards a further 18% appreciation by mid-2020. The high spot-vol correlation should bring about a large increase in gold vol, see the following report for more details.

Hence, we advocate adding longs in 9M 25D at the money gold call options at 15.54 vols, indicatively.

Alternatively, on hedging grounds, we advocated long positions in August month’s CME gold contracts. We now like to re-initiate the same strategy by adding longs in CME Futures contracts for December’19 delivery as we could foresee more upside risks amid global financial crisis.

Buying interests are mounting on safe-haven sentiments amid global slowdown which is still imminent. Courtesy: Sentrix, JPM & Saxobank