China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

on shrinking vols before risky event - EconoTimes)

Market focus to remain on 23 June referendum, this week is devoid of policy news but, of course, the markets will continue to follow closely the news on the forthcoming 23 June referendum.

Manufacturing output looks set to stumble again and the RICS housing survey should confirm the trend of cooling price pressures.

Aussie prints upbeat trade balance numbers and GDP (QoQ), trade deficit has been contracted from previous -1.97B to the current -1.58B, while GDP on quarter in the March of 2016 has been expanded 1.1% from the previous prints of 0.7%, whereas U.K. construction PMIs have missed the estimates, actual 51.2 versus forecasts at 51.9.

The monetary policies from RBA tomorrow and BoE in next week are likely to be unchanged, but we reckon that UK referendum is likely to add volatilities in the FX markets post event.

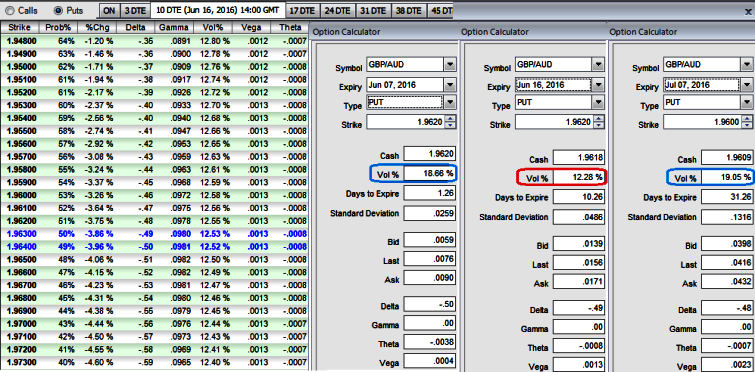

BoE's rate decision would be released next week which is likely to remain unchanged but the potential Brexit event keeps adding more pressures on sterling. But referring to above diagram for IVs of various tenors in FX options owing not only to the referendum but also the U.K's interest rate speculations.

With resultant effects, the GBPAUD cross is anticipated to depreciate further, most likely towards 1.93 levels in the near terms.

Since OTC markets seem to be highly turbulent with an extremely bearish environment post-Brexit decision, IVs for 1M contracts are expected to spike (tad above 19%). This would be good news for long-term option holders contemplating the prevailing bearish environment but more number of longs in ATM delta puts would ensure the reasonable probabilities in underlying exposures.

To factor in the weakness in this pair as we could see reasonable IVs even in next 1-3m expiries, we recommend capitalizing more on bearish signals both fundamentally as well as technically, employing OTM longs matching with ATM longs to construct back spreads that likely to fetch positive cash flows.

Please be sure that a large move in the underlying should be allocated with longer tenor (targets set below 1.93 levels or 1.8838 levels). This should be of greater concern than doing the spread for reducing debit.

So, here goes the strategy this way, go long in 2 lots 1M ATM -0.49 delta puts, long in 2M (1%) OTM -0.36 delta put, and simultaneously short 1W (1%) ITM shorts, the spread is to be executed in the ratio of 3:1with net delta at around -0.72

The delta of the strategy is at 72%, which means there is more likelihood of expiring ITM, since we are certain about our research, we preferred 1 lots of extra long of slightly OTM strikes in our Put Ratio Back Spread.