China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

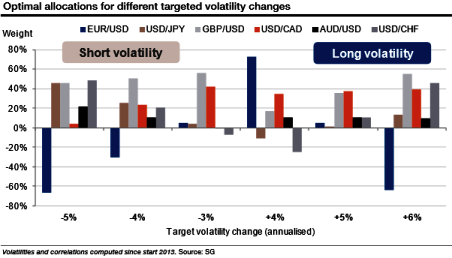

Targeting volatility via optimal portfolios:

An aggressive trader or investor keen on the volatile asset class targets a rise or fall measured in volatility points.

However, the Markowitz framework can be used to design optimal allocations which correspond to the volatility change targeted by the investor.

The main observations on the six optimal allocations obtained with the data sample since the start of 2013 follow below (see graph):

AUD/USD volatility generally has a small weight while the EUR/USD and GBP/USD tend to have large absolute weights.

All allocations (buying and selling volatility) are buying GBP/USD and USD/CAD volatility.

Long volatility portfolios are underweighted in USD/JPY volatility.

Targeting either a large rise or fall involves massively selling EUR/USD volatility and buying the five others.

The biggest long USD/JPY volatility exposure is found to target a large volatility fall.

The corresponding portfolio will be efficient in the sense that it will be diversified and exposed to the minimal level of risk given the targeted return. In that way, the expected return becomes an exogenous input.

Obtaining the optimal allocations equates to a slide on the efficient frontier. We compute the optimal allocations corresponding to targeted volatility increases and falls. The order of magnitude of these investing scenarios corresponds to the historical scenarios.

The numbers reflect the usual asymmetry with volatility increasing more than it falls (the return of the naive allocation is a gain of 4.9 points in the rising case, whereas the falling case sees a gain of only 4 points).