J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts

Today, USDCNY mid-point fix was set just slightly lower at 6.9098 and is holding steady around 6.9300. The Chinese fiscal policy may need to remain expansionary to offset any tightening in credit conditions that may arise from the regulatory changes. This brings us to the currency. The potential regulatory changes are yet another source of uncertainty for overall conditions and where PBoC would like to take it. In the end, stability is probably the best option for now.

The long SGD and THB FX positions have been squared-off against the USD over the past ten days on the assumption of an adverse US-China trade conflict. We, though, continue to shy away from being short these currencies or for that matter KRW and TWD given the starting point of current account balances and valuations. CNY FX is different to these other currencies in that it does not enjoy the aforementioned supportive factors any longer. In an adverse trade war, CNY will likely bear a part of the policy adjustment.

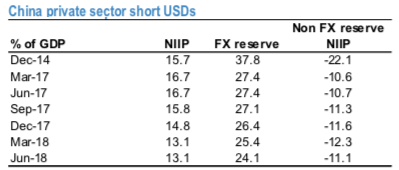

A bounded trade expression: Accordingly, a paid 3x6 CNH forward position is activated (180 pips vs 3mth outright at 315pips). The private sector is short USDs even though some of the imbalances moderated in 2Q’18 (refer above chart) and higher capital outflows could cause forward points to rise as has been the experience in 2015 and late 2016 / early 2017. Our trade expression is a bounded one and not an outright short CNY one because every base-line scenario carries a tail risk and there is always a possibility that the trade tensions moderate in intensity or are spread over time. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly CNY spot index is flashing at -42 (which is bearish), while hourly USD spot index was at -78 (bearish) at 13:13 GMT. For more details on the index, please refer below weblink: