Bitcoin Sheds $491M in ETF Outflows and Retreats Below $64K; Sellers Reload for $50K

Bitcoin Sheds $491M in ETF Outflows and Retreats Below $64K; Sellers Reload for $50K  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110

AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110  ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break

ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break  FxWirePro: USD/ZAR slips as dollar weakens after PCE inflation data

FxWirePro: USD/ZAR slips as dollar weakens after PCE inflation data  BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts

BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts  FxWirePro: USD/CAD uptrend loses steam, remains on bullish path

FxWirePro: USD/CAD uptrend loses steam, remains on bullish path  FxWirePro: NZD/USD extends losing run, eyes 0.5600 level

FxWirePro: NZD/USD extends losing run, eyes 0.5600 level  FxWirePro: GBP/USD heads deeper into bear territory, 23.6% fibonacci eyed

FxWirePro: GBP/USD heads deeper into bear territory, 23.6% fibonacci eyed  FxWirePro: USD/CAD hits 14-month high , Scope for further upside

FxWirePro: USD/CAD hits 14-month high , Scope for further upside  FxWirePro: GBP/AUD edges higher but bullish outlook persists

FxWirePro: GBP/AUD edges higher but bullish outlook persists  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: AUD/USD drifts lower, uninspired by jobs beat

FxWirePro: AUD/USD drifts lower, uninspired by jobs beat  FxWirePro: USD/JPY dips as Japanese Yen consolidates near 40-year low

FxWirePro: USD/JPY dips as Japanese Yen consolidates near 40-year low  FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet

FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet  FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop

FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop

It is unlikely to regard EURO's sustainably higher until there is real domestically generated inflation.

Headline inflation has been dragged down by energy prices but even core inflation is soft (particularly in Spain/other periphery countries).

Services inflation appears to have troughed but is yet to trend higher (services are 43.5% of consumption basket and depend more on domestic factors/wage pressures).

Eventually we think EUR recovers but it will be slow. However, these speculations have left the forecasts unchanged in this month (EUR/USD 1.03 end-Q1 and parity by end-Q2).

Hence, EURO could be boosted temporarily by risk aversion in its role as risk off proxy or more sustainably by signs of inflationary pressures.

Hedging Frameworks:

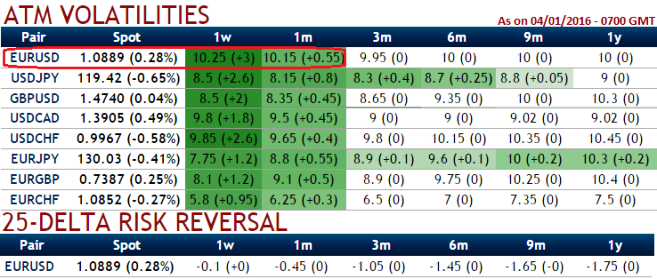

As you can observe from the table showing implied volatilities of ATM contracts (EURUSD of 1W-1M expiries show 10.25% and 10.15% that is the highest among G10 majors).

So, by employing the Vega options can not only multiply the returns but also upbeat the implied volatility.

Any spikes in this pair in near term can be attributed as shorting opportunity in our back spreads.

As shown in the diagram, contemplating the above risk reversal computations, we construct strategy comprising of both ITM as well as ATM puts in the ratio of 2:1 so as to suit the swings on either directions.

Capitalizing on higher IV and negligible risk reversals in short run, we can eye on shorting (0.5%) 3D in the money put that would lock in certain yields by initial receipts of premiums.

Thereafter, 2 lots of 1m ATM -0.48 delta puts with vega 124.62 are preferred to suit the prevailing losing streaks, thereby the spread would be executed for net debit and the cost is reduced by short side.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: EUR/USD tops IVs among G10, deploy vega puts in diagonal back spreads for tight hedging

Monday, January 4, 2016 1:22 PM UTC

Editor's Picks

- Market Data

Most Popular