Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

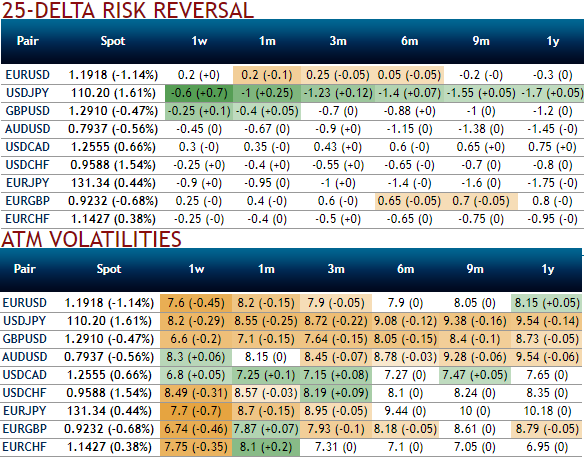

Please be noted that the implied vols of euro crosses have been shrinking lower in spite of the series of data flows are lined up.

German retail sales (actual -1.2% versus consensus -0.5% and previous 1.1%), German and Italian unemployment claims, Euro area unemployment and inflation numbers are due to be announced shortly.

EUR vols and bearish neutral risk reversals remain low compared to the level of rates. Also, in longer tails, the EUR volatility smile remains flat compared with the rates vs vol correlation seen since 2015 and over the past week.

The steepness of the EURJPY risk-reversal curve renders back-end tenors better shorts, risk reversals have been bearish neutral. While positively skewed IVs towards OTM put strikes signifies hedgers’ bearish sentiments but puzzles prevailing uptrend of euro.

However, we prefer sticking to 2017 expiries (6M) since 2018 dates come with unpredictable Italian election risk. The EUR/gold risk-reversal curve is much flatter in comparison hence short tenors work fine. We enter short 6M 25D EURJPY risk-reversals (delta-hedged).

We advocate maintaining the bullish exposure in EURJPY via a call RKO as JPY weakening is likely to be a slow grind rather than explosive.

Sell 6M EUR/JPY 25D risk-reversal (buy EUR calls - sell EUR puts), delta-hedged.

Vol pts Positive smile theta participation in Euro bull-trend.

The macro theme of euro area leading outperformance remains dominant; maintain core EUR or proxy longs as growth and inflation data continue to be supportive. Accordingly, encourage long EUR vs in cash (vs USD) and through options in EURJPY (131 call, RKO 135).

Any spot holdings, wise to book returns in long EURJPY cash; but stay long EURJPY in options structure.

A key judgment call in G10 is to separate those central banks that have the potential to change policy in the near term from those that are unlikely to do so. The BoJ is firmly in the latter bucket and its yield targeting framework have left JPY as having the highest beta of any other currency to DM yields.

The short JPY leg of these trades has thus been motivated by its sensitivity to higher yields. We still recommend keeping exposure to long EURJPY trades but think that the move will likely be a grind higher rather than an explosive move that one might expect if the Fed weren’t on the side lines and US yields were moving higher as well. Thus we take profits on the cash version and keep exposure through the EURJPY call RKO to participate in the dubious bull run.

Currency Strength Index: FxWirePro's hourly EUR spot index is flashing 79 (which is bullish), while hourly JPY spot index was at -63 (bearish) at 07:00 GMT. For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: